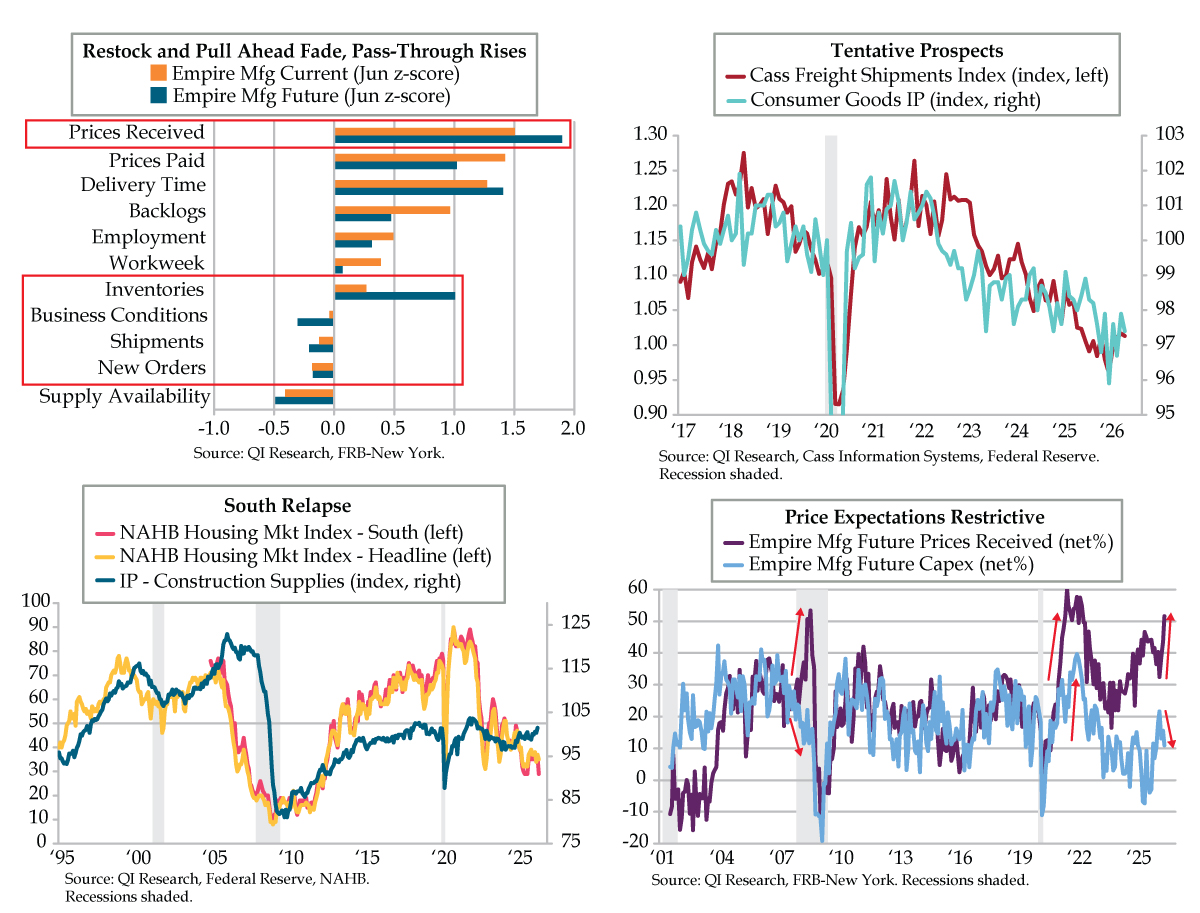

QUICK QUILL — June’s Empire Manufacturing report had two takeaways: 1) Inventory restock and demand pull-ahead fading and 2) Cost pass-through to factory gate prices rising. While Fed doves may take solace from slower growth rumblings, higher inflation expectations will embolden the hawks going into tomorrow’s policy decision. The Fed’s ‘Higher for Longer’ policy continues to buffet sectors like consumer goods and home building. Now ‘Higher for Longer’ price expectations are hampering the Second District capex outlook. This dynamic is not the Fed’s doing, but it echoes the Great Recession and questions whether an “unchanged” decision tomorrow is the right one.

TAKEAWAYS

- NY Fed Empire Mfg Current Delivery Time, Current Prices Paid, and Current Prices Received all printed above a +1.5 z-score for the first time in May, excluding COVID; Future Prices Received surged to a +1.9 z-score, the highest of all 23 subcomponents

- After rising 6% this year from January’s cycle low through April, the Cass Freight Shipments Index fell 0.3% MoM in May; while Consumer Goods IP has risen off January’s cycle low as well, it remains weak, a sign of Higher for Longer impacting more rate-sensitive sectors

- The NAHB’s Housing Market Index came in two points below consensus at 35 and has been below 40 for 14 months running, a streak not seen since 2011-12; in particular, the South, which accounts for 60% of new home construction, sank to a nine-month low of 29