“He’s taking a pretty big lead out there, almost daring them to try and pick him off. The pitcher glances over, winds up and it’s bunted. Bunted down the third-base line. The suicide squeeze is on. Here he comes, squeeze play, it’s gonna be close. Here’s the throw, here’s the play at the plate. Holy cow, I think he’s gonna make it!”

R.I.P. Meat Loaf. But his music will live on. This excerpt from the timeless rock opera “Paradise by the Dashboard Light” off the 14 times platinum Bat Out of Hell album was delivered by legendary Yankees shortstop, Phil “The Scooter” Rizzuto. We do want to clarify any ‘confusion’ that Rizzuto often claimed to not get the innuendo behind his part of the song about teenage lovers in a parked car. In 2007, Meat Loaf told ESPN, “Phil was no dummy – he knew exactly what was going on, and he told me such. He was just getting some heat from a priest and felt like he had to do something. I totally understood. But I believe Phil was proud of that song and his participation.”

“Stop right there…!” Ellen Foley, who sang the duet with Meat Loaf, blasted out that next line immediately following The Scooter’s recording. That was what resonated after seeing January’s IHS Markit’s U.S. Flash PMI (purchasing managers’ index) yesterday.

A quick glance revealed the authors dismissed the disturbance in the data as an outlier tied to Omicron. The implication: A bounce back is imminent and inevitable. With deference where due, surprising weakness is still just that until proven otherwise. To take but one example, we find nothing aberrant in Markit’s manufacturing output index plumbing a 19-month low of 50.3. At 49.6, it would be equally superficial to shrug off the factory sector’s employment index posting its first contraction since July 2020. Backing the need to employ fewer warm bodies to work down backlogs were…backlogs which have posted a four-month cumulative compression of 8.1 points, the magnitude of which was seen in the last two recessions.

The Street knows that IHS Markit’s business survey data has long played second fiddle to the longer running ISM (Institute for Supply Management) report. We happen to be partial to the series given it reflects broader macroeconomic breadth by casting a wider net. Moreover, another entity under the IHS umbrella produces a GDP tracking model that’s best in class gauging the current quarter’s growth momentum.

Formerly known as Macroeconomic Advisers, the group’s crack economists cut their 2022 first-quarter gross domestic product estimate by four-tenths from 2.4% to 2.0% following the Flash PMI’s release. Contrast that with Bloomberg’s 3.0% consensus. Per IHS, the 50.3 print was the lowest since June 2020 and, “indicative of less goods GDP in January than was implicit in our previous GDP tracking for the first quarter.”

Dr. Gates reached out to the team and discovered that this metric is used as a check against their own goods GDP model, especially when there are outlier moves. What’s unique is the seldomness of this manifestation – as relayed, the economics team can count on one hand the number of times the PMI changed their tracking. That’s unusual and significant all at once.

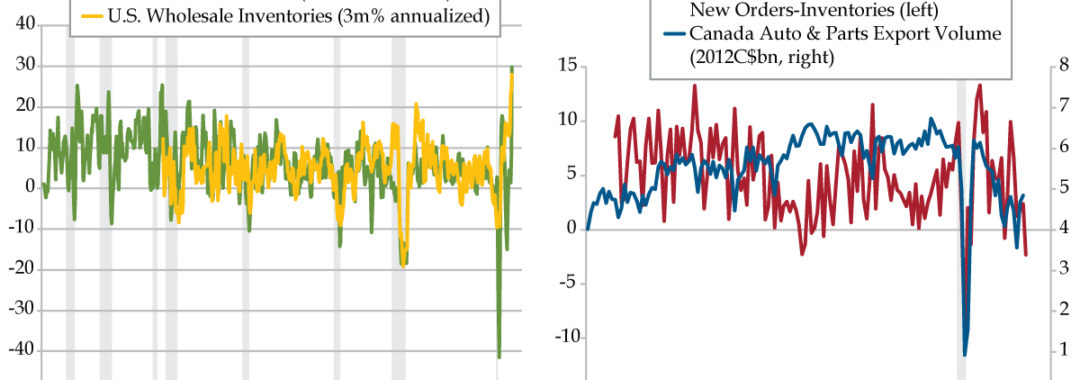

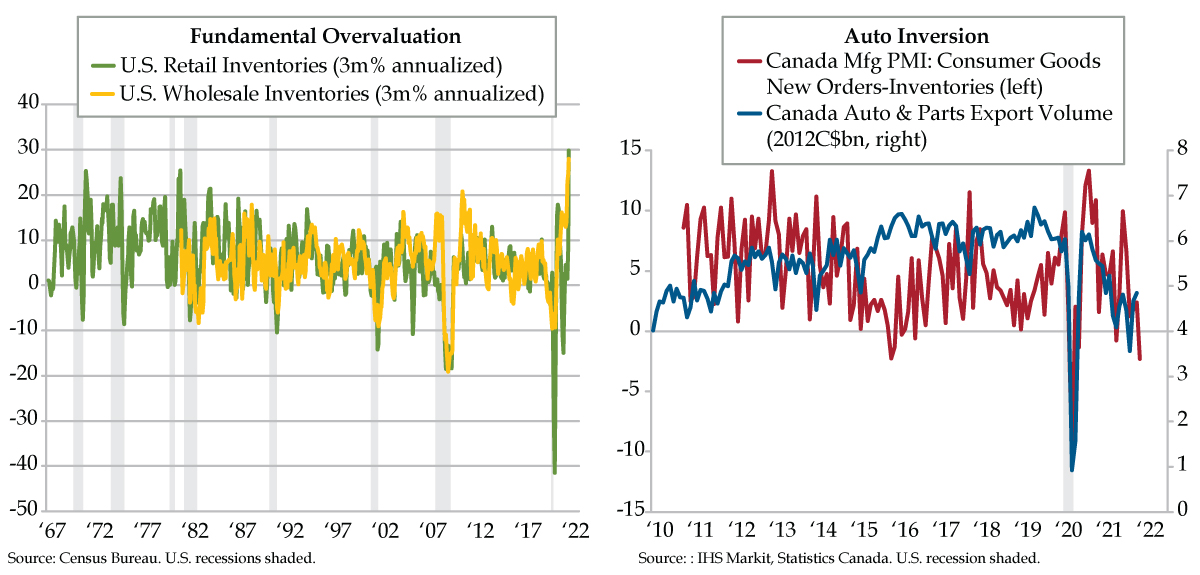

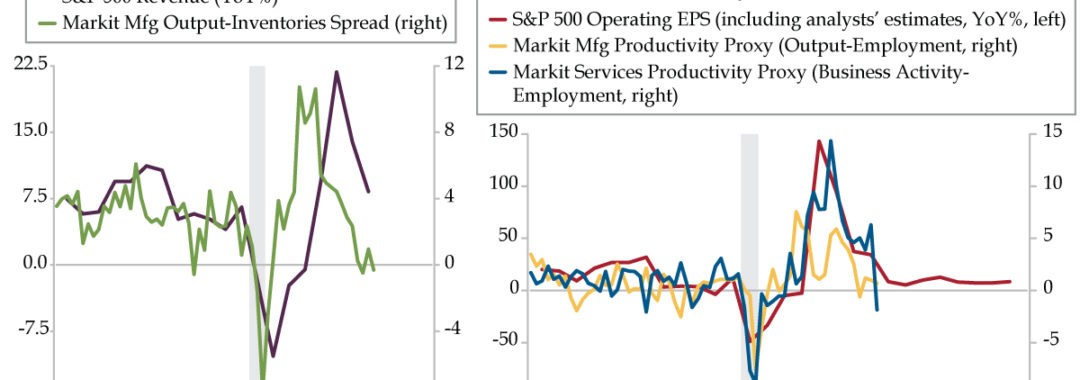

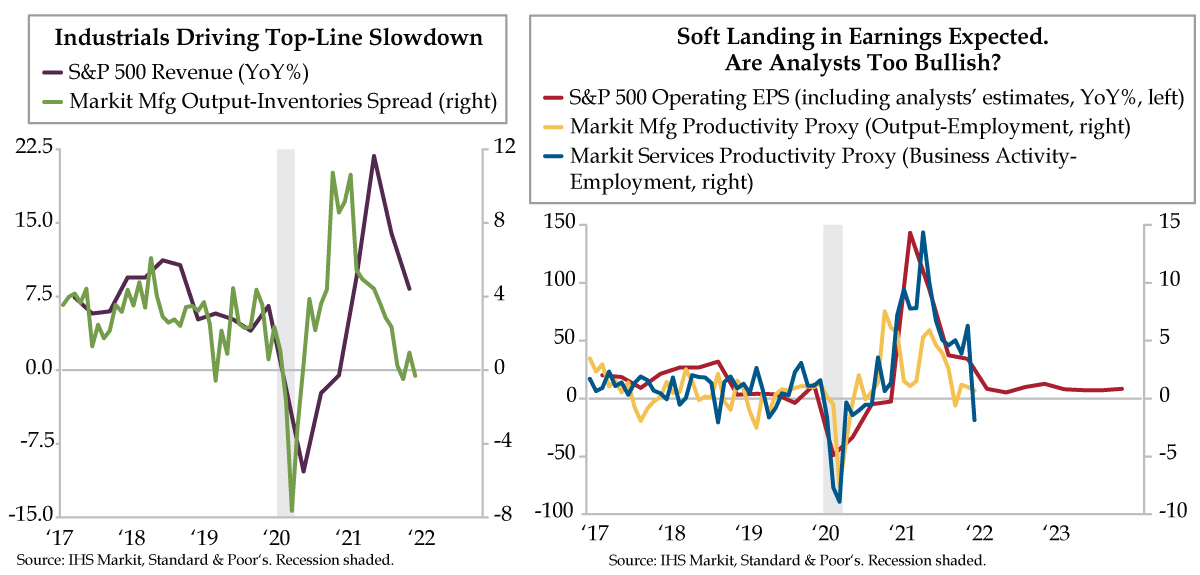

Omicron or not, top-line growth is slowing abruptly to kick off 2022, driven by the cyclical industrial sector which casts skepticism at the expected path of S&P 500 revenue growth (purple line). Short-run guidance is provided from a coincident-to-lagging comparison in the manufacturing PMI. Through January, the Production-Inventories (of inputs, not finished goods) spread posted the second inversion in three months (green line). Recall that inversions are triggered when demand runs below supply, as was the case in November and January. The expectation is that growth will slow in the near term.

Stalling industrial output implies burgeoning impediments to growth outside the confines of the factory sector. As it happens, productivity proxies suggest a downshift is in the makes in corporate earnings. The manufacturing output-employment spread (yellow line) and services business activity-employment spread (blue line) stand as illustrations to the premise.

According to analysts’ estimates collated by Standard and Poor’s, S&P 500 operating earnings per share (EPS) are poised to moderate through 2022’s second quarter and then expand at a quiescent pace through yearend 2023. The compression in productivity proxies, first for manufacturing and now more visible for services, suggests the storied soft landing in earnings is at risk and that (shockingly) analysts might be too bullish.

Granted, all eyes are on Wednesday’s Federal Reserve meeting. As we tweeted out yesterday, it wouldn’t surprise us if Fed officials had a big screen TV rolled into that massive room in the Eccles Building to watch the action these next two days. They’d be joining stock jockeys and overnight technicians who are hyped up about stocks’ history-making Monday turnaround. We too stood witness in wonderment.

As amazing as it was to watch, violent volatility cannot detract from evidence of a slowing in economic activity to a 2% annualized rate in the first quarter, within spitting distance of the longer run 1.8% growth pace. Further deterioration risks the U.S. expansion slipping below trend. That’s when the aberration of a contraction in Markit’s labor market reading becomes the norm.

“Holy cow!” Philip Francis Rizzuto, God rest his Hall of Fame Yankees soul, would channel his best radio announcer persona and tell us that here it comes, squeeze play, top line and bottom line, it’s gonna be close. From one paison to another, you ain’t kidding, Scooter.