VIPs

- QI forecasted strong January ISM New Orders, but the rebound’s durability is in question; a positive ISM anecdote on the leading global chemicals sector and the breadth of global manufacturing PMI new orders-to-inventories spreads bode well but pre-date coronavirus

- Two key hard data trends – the manufacturing workweek and industrial production — must turn decisively bullish to confirm the positivity in the ISM and global PMIs; the combination of the coronavirus and the collapse in global transportation could derail the nascent recovery

- The historic volatility of the PMI new orders-to-inventories spread suggests it wouldn’t take much to reverse the move; a re-strengthening in crude oil prices via stronger global demand, however, would validate this positive signal and green flag the momentum trade

If you grew up in the 1970s, you had no choice but to watch television commercials, unless, of course, you left the room to get a snack. At least the advertising agencies of that era came up with catchy jingles and memorable marketing magic to fill the small screen. Remember Mikey from the Life Cereal commercial? Or Mean Joe Greene from the Coca-Cola ad? Budding future Wall Streeters recall another commercial for the stock brokerage founded by Edward Francis Hutton and his brother, Franklyn Laws Hutton. Its slogan remains etched in our collective memory: “When EF Hutton talks, people listen.” EF Hutton had some serious Street cred back then. For several decades, it was the second largest brokerage firm in the country.

Investors listen to bellwethers. And while WHO and CDC may be more important acronyms at the moment, ISM (short for Institute for Supply Management) always carries weight in judging the fundamental backdrop.

Before delving into January’s report, a quick note on ISM’s survey period. Though the Institute generally sees respondents wait until late in the month to submit their perspectives, there was nary a word on the coronavirus in yesterday’s release. We’ll have to wait for February’s survey to get a cleaner read on the damage to the global supply chain.

The better-than-expected January ISM report initially triggered a three-basis point intra-day jump in the U.S. 10-year Treasury yield. And then traders bought the dip. To be sure, the headline index, New Orders and Prices Paid all came in above the market’s, but not our, expectations. January 27th’s Feather flagged the rebound in New Orders (you’re welcome). And yet, like those doubtful bond traders, we recommend you curb your enthusiasm. We’re not sold on the durability of this green shoot.

ISM’s Customers’ Inventories index checks-and-balances New Orders. When it leans “too low,” restocking is the (re)order of the day and vice versa. Enter December Customers’ Inventories, which fell to a 10-month low of 41.1 and flagged the rebound in New Orders. The January uptick in Customers’ Inventories to 43.8 suggests February’s New Orders impulse won’t be as strong as January’s 52.0. Backlogs, or future demand, did improve but remained in contraction corroborating the potential for a chillier February.

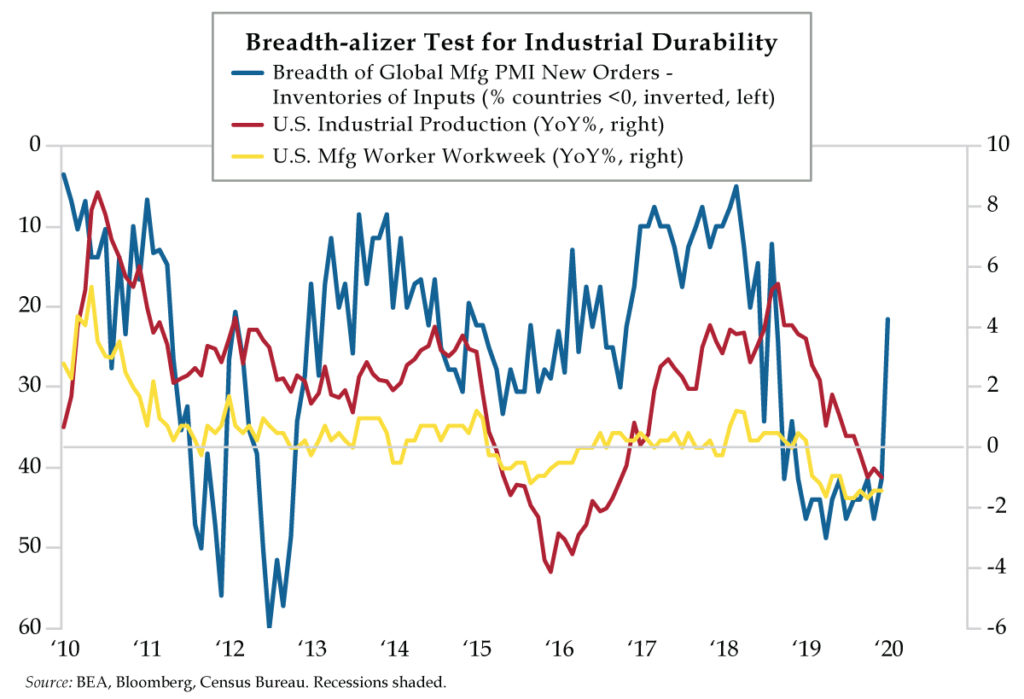

Stepping out to the global picture, we can’t help but be encouraged by an anecdote in yesterday’s ISM as it pertained to our favorite leading cyclical industry: there are “small signs of increased global demand in the chemical segment.” The breadth of global manufacturing purchasing managers’ indices (PMI) new orders-to-inventories spreads backs this nascent sign of future strength.

We track this short-run demand/supply guide to industrial output across forty-one countries, thirty-seven of which had been reported for January, a month in which the percentage of countries with new orders-to-inventories below zero (excess supply) fell to 22% from December’s 41%.

Inverted above in blue, this breadth-alizer test reveals a burning desire to restock. It’s flashing a strong, but tentative, bullish signal for two key cyclical indicators – the manufacturing worker workweek, one of 10 feeders to the U.S. Leading Index, and industrial production, one of the four horsemen of the business cycle used to date recessions by the National Bureau of Economic Research.

The durability of the global reflation narrative HAS TO translate from the soft data signal (breadth) to hard data trends (manufacturing workweek, industrial production) for us to turn decisively bullish on global growth and the long-cyclicals trade. Today’s chart shows this breadth metric leads turning points in factory worker hours and industrial output. But any number of hiccups could derail a rebound. To that end, there was no validation of building strength in manufacturing payrolls given January U.S. employment index remained in negative territory.

That’s where Coronavirus and Dow Theory intersect. The outbreak will slow Chinese industrial activity for longer than usual during the seasonally slower Lunar New Year period. And transports will be hammered as outbound port and air freight volumes are curtailed until further notice – or at least until the containment quotient is great enough to fire up production again. You’ll know it when you see it in crude oil prices.

Mind you, pre-coronavirus, U.S. transports was still on its back which was reflected in yesterday’s ISM commentary of, “continued signs of a slowdown in manufacturing” from the Transportation Equipment sub-sector.

Our breadth-alizer has higher volatility than the two pillars of industrial activity – workweek and production. That means it wouldn’t take much for future PMIs to backslide turning a bullish January into a bearish February and (even) March.

One month never makes a trend, especially given the risks to February’s data from the coronavirus. Best not to jump to conclusions from one ISM survey or round of PMIs, even if EF Hutton was doing the talking.