The country was in mourning as was its young Queen, who was not to be coronated until the following June to allow ample time for her bereavement at the passing of King George VI, who died in his sleep on February 6, 1952. By the end of that year, London would be blanketed in a different kind of grief. Being situated in a large river valley as it is, air circulation is limited in the city. On December 5th, an anticyclone, a high-pressure weather system, trapped warm air below a mass of cold air that surrounded London. Densely populated and solely reliant on coal for heating, a thick layer of smog born of chimney smoke filled with sulfur dioxide and car exhaust fumes entombed the city. Visibility was reduced to a few yards, public transport ceased operation, including ambulances. In the space of four days, an estimated 4,000-12,000 died from respiratory infections in the worst environmental disaster in UK history. The subsequent Clean Air Act of 1956 required smokeless fuels to be used in heavily populated areas and became the benchmark for subsequent laws worldwide.

By that time, the Queen was working with Winston Churchill’s successor, her second of what would be during her reign, 15 prime ministers, Harold Macmillan. Inflation had fallen a touch to 5.1% from 1952’s rate of 5.3%, which compared to the U.S. Consumer Price Index (CPI) of 1.5% that year. Tomorrow’s CPI is expected to fall to 8.0% from July’s 8.5%, while that of the UK will follow Wednesday; it’s forecast to tick down to 9.9% from 10.1%. The Bank of England’s postponement of its Monetary Policy Committee meeting to September 22 will give it more time to deliberate with the benefit of GDP, Retail Sales, and Unemployment data in hand. They will also have the fiscal statement in hand, which could sway policymakers to push for a 75-basis-point (bp) hike.

Across the pond, the Brits’ American peers at the Federal Reserve effectively pre-announced a 75-bps hike will be delivered a day earlier via a Wall Street Journal article penned by the central bank’s presumed mouthpiece. At least Fed officials dignified blackout, which won’t end until after they meet next Wednesday, by having the story plant released before being gagged – progress we applaud.

When Jerome Powell does take the podium, we expect he will emphasize the continued heat in the core CPI, which is expected to have ticked up to 6.1% last month from July’s 5.9%. Blame the lagged manifestation of house prices and rental inflation in the data. Powell will also lament the overly hot labor market and retail sales data. Subjects to be avoided include the largely healed supply chain, the contraction in real-time job postings data we shared Friday, the record evisceration of net worth in the second quarter, the continued explosion in credit card spending, a housing market correction that’s unfolded in half the time it did the last time the bubble burst, and especially GDP.

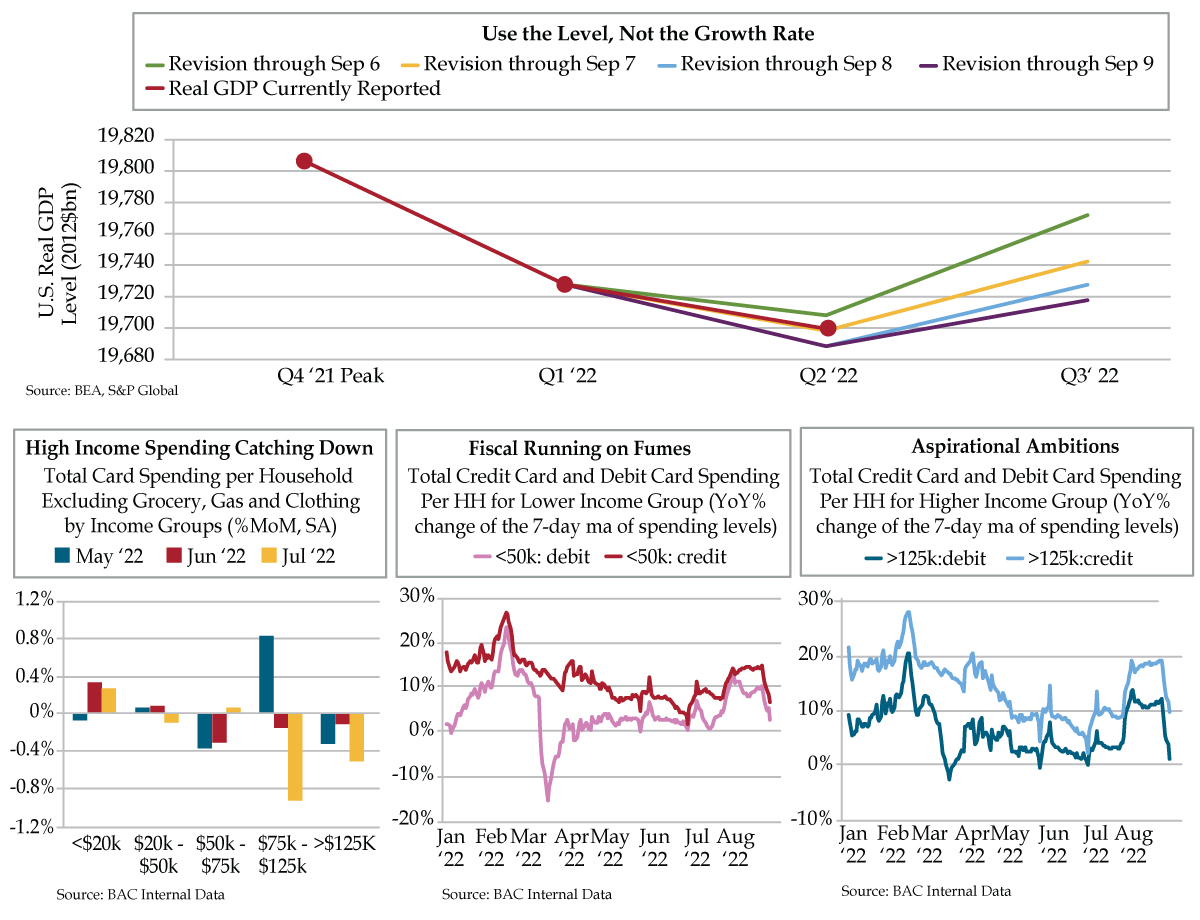

On that last count, QI’s Dr. Gates noted Friday that S&P Global’s taking its third-quarter GDP growth forecast down two-tenths to 0.6% renders it inadequate to offset the -0.8% clocked in the second quarter. That would leave the dollar level of GDP below 2021’s fourth quarter peak as the momentum could not reverse the second-quarter losses; the level would also be below that of 2022’s first quarter (top graph).

“This is important because of how recessions are scored, by the level of GDP, not growth rates,” Gates explained. “Past recessions have included quarter-over-quarter gains in GDP that were surrounded by negative quarters. If third-quarter estimates stay positive and the data print that way, it will not mean that the recession has ended even though that is what myopic markets will conclude. That would become the crowded view and you can’t fight that view. ‘Recession not over’ would become the value trade under this scenario.” The arbiters at the National Bureau of Economic Research would confound investors conditioned to follow growth rates by calling recession when most will assume we’ve dodged that development.

The economists at Bank of America predict Thursday’s Retail Sales report for August will raise GDP estimates for the third quarter. “We expect the core control group — retail sales ex auto, gas, building materials and restaurants — to increase by 0.8% month-over-month,” they wrote Friday. That compares to Bloomberg’s consensus estimate of a gain of 0.5% for core sales, the component that feeds GDP estimates.

Last Thursday, we learned that credit card debt had risen by $10.9 billion in July to $1.14 trillion. The three BofA charts we share depict a continued rise in credit card spending across the income spectrum offsetting a flatlining in debit card spending. Critically, in July, spending contracted for a third straight month among those earning more than $125,000 (bottom left chart).Debit card spending growth within that same cohort is on the brink of turning negative; the same cannot be said for putting it on plastic, where growth remains in the double-digits (bottom right chart). A similar dynamic is at work for those earning less than 50% (middle bottom chart). The best way to cease spending at the top, which accounted for 49% of the growth in 2021 consumption, is a stock market swoon. You don’t need the smog to clear to see that June’s stock market lows coincided with the last time those credit cards were put away (light blue line).