On August 20, 1911, a man entered the poorly secured Louvre Museum. As recounted by NPR, that morning, “Vincenzo Peruggia, an Italian handyman who had briefly worked at the Louvre, donned his old uniform, walked into the museum and, when the coast was clear, took the painting right off the wall. He slipped it out of its frame in a nearby stairwell and carried it out of the building underneath his smock.” In a twist, Peruggia got stuck in said stairwell. Whilst attempting to disassemble the doorknob, a Louvre plumber appeared, who, rather than apprehend him, helped him open the door. With a friendly thank you, the robber made his getaway. Two years later, Peruggia attempted to fence his treasure to a Florentine art dealer, Alfredo Geri. After conferring with Uffizi Gallery director Giovanni Poggi, a meeting was set in Peruggia’s Florence hotel room. There, the thief produced the marvelously preserved Mona Lisa, confident he was restoring “her” to rightful ownership. The Florentines agreed to the 500,000-lire price and immediately arranged for ‘her’ to be taken to the Uffizi. Post-authentication, the theft was reported, and on December 11, 1913, the Italian “patriot” was arrested at his hotel.

Some would argue that security still plagues the world-famous museum. At 9:34 am Paris time this past Saturday, posing as workers in a nod to Peruggia’s legacy, thieves made off with priceless Napoleon-Era jewels in seven minutes flat. It was yet another humiliation to France, which is fraught with political instability. Germany can attest as France is its largest trading partner in the Euro Area and generating a sizable amount of uncertainty for its export outlook.

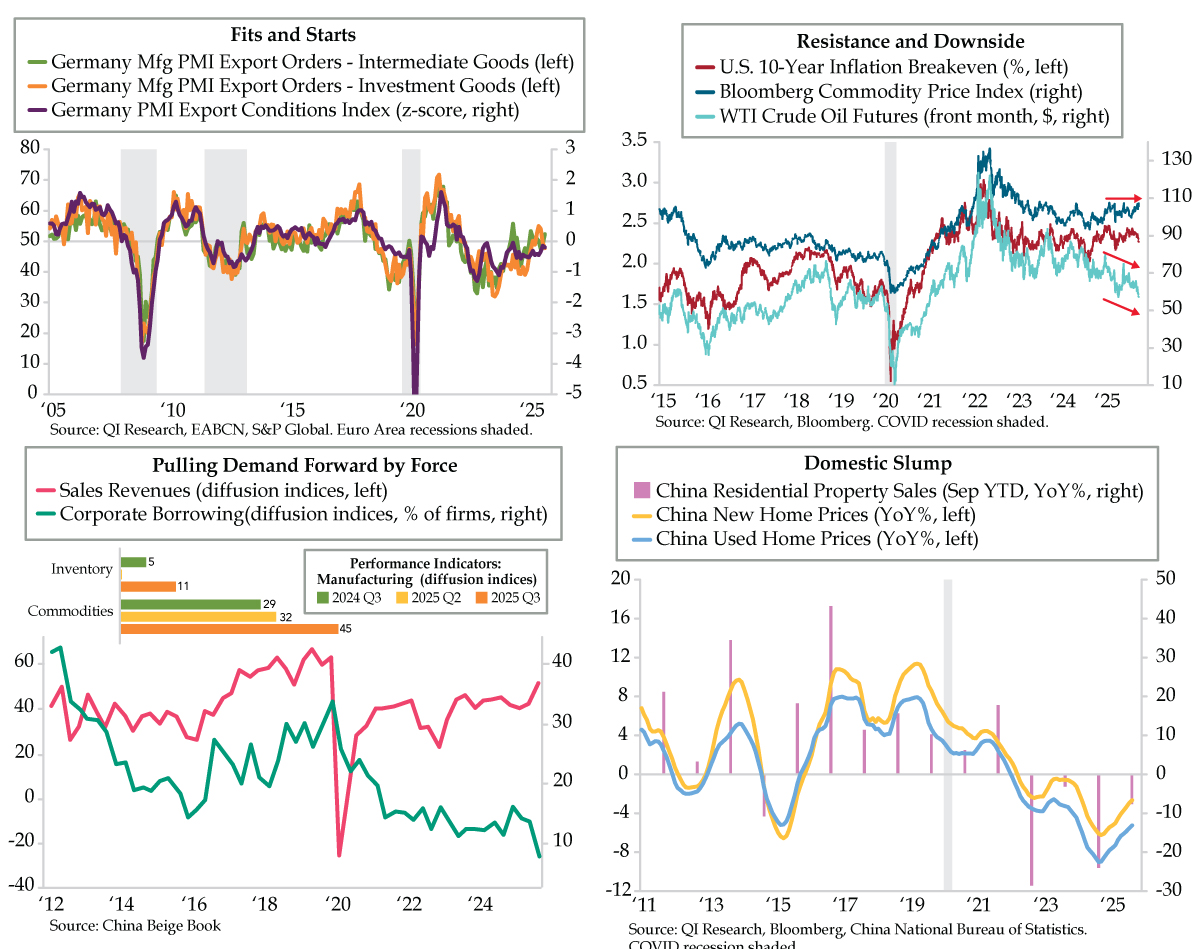

The Hamburg Commercial Bank (HCOB) Germany Export Conditions index ticked down to 51.3 in September from August’s 51.5. While above the breakeven 50-level, it ran below the 52.1 long-run average for the 41st consecutive month, the longest slump for German exports since the series’ 2005 inception. Extraordinarily, the latest below-normal streak combines the respective 16-month and 25-month stretches from the 2008-09 Great Recession and the 2011-13 Euro Area Recession.

Standardizing the Export Conditions Index on a z-score basis (purple line) puts the 3-plus-year run into perspective. The post-COVID global supply chain normalization reliably guides Germany’s manufacturing purchasing managers’ index (PMI) for New Export Orders of Investment Goods. However, the recent run for this gauge to June’s high of 54.9 was short-lived as the measure fell back to September’s 47.8, a seven-month low (orange line).

Farther upstream, Germany’s New Export Orders index of Intermediate Goods has put in fits and starts, echoing below-normal export conditions. Both runs at escape velocity have failed – once in May 2024 at 55.7 and again in February 2025 at 53.3 (green line). At 52.4, September marked the third test, but we’re inclined to grade it ‘incomplete’ at this juncture. As HCOB/S&P Global noted, the spurt of activity “mainly reflected a faster economic upturn in Mainland China during the latest survey period.”

Here, Bloomberg’s Commodity Index (ticker BCOM), covering 22 commodities from agriculture, energy, livestock and industrial and precious metals sectors, enters the narrative. Recent trading echoes the tentativeness of Germany’s export orders of intermediate goods. Since May 2024, including this week, BCOM has tested the 107-108 range four times (blue line). The role played by gold and silver is clear. West Texas Intermediate (WTI) crude oil is broadcasting an entirely different message – this global growth barometer has seen futures prices break below the $60 per barrel mark for the second time this year (aqua line). How do you think that’s going to sit with the 90% of 136 oil and gas executives, polled in the third quarter Dallas Fed Energy Survey, who expect WTI to end 2025 at $60 or higher? Moreover, any additional breakdown in WTI would weigh on rangebound U.S. 10-year breakeven inflation (red line), and hence, nominal U.S. 10-year yields.

As for Germany’s Middle Kingdom boost, QI’s friends at China Beige Book (CBB) corroborated as much in their third quarter report. Ditto on the commodities front given China is the world’s marginal buyer of commodities. On that note, per the CBB, Sales Revenue improved over the quarter and over the year to a new cycle high (fuchsia line). Despite the “upbeat” outlook, CBB cautions that the top-line performance reflected demand pulled-forward by force as factory activity was driven by a jump in Inventories (11 in Q3, orange bar inset). As such, industrial firms could face “oversupply by early 2026.” As for what drove the restocking, “Commodities’ inventories didn’t just rise in Q3, they skyrocketed. There’s little reason for the Commodities mini-boom to last and, when it ends, Manufacturing will be more vulnerable.” So will commodities prices worldwide given they posted “the strongest growth seen since 2019” (45 in Q3, orange bar inset).

Even as China’s third-quarter 4.8% year-over-year (YoY) GDP growth was the slowest in a year and despite Wall Street clamoring for big stimulus, CBB cautioned against irrational enthusiasm: “A true recovery should encourage firms to ramp up operations, including borrowing. Instead, nearly every credit indicator we have is tanking. Borrowing nationally hit a record low [teal line], and underneath the hood the view is even worse: every firm size saw borrowing fall, as did both private and state firms, as did every region and every sector save commodities.”

China’s disinflationary factory-led payback will collide with ongoing deflation via its protracted housing slump given: 1) demand is weak; 2) supply is rising; 3) prices are falling. Year-to-date through September, home sales were down 7.6% YoY, a fourth contraction in as many years (lilac bars). Adding punctuation, CBB added that “inventory of unsold homes jumped sharply.” Both new (-2.7% YoY, yellow line) and used (-5.2% YoY, light blue line) home price trends continued to contract. China and Germany are combining forces to heist the upside potential in inflation.