Most major blackouts are the result of cascading failures, storms or even equipment meltdowns, but there have been instances where human error caused a massive collapse – like what happened in Taiwan in March 2022. A failure at the Hsinta coal-fired power plant in Kaohsiung led to blackouts across multiple regions, including the capital Taipei and parts of the chip-making hub. A maintenance team at the power company had removed insulating gas from a circuit breaker at the plant and warned operators not to route electricity through the equipment. Despite a yellow and red warning notice that read “Do Not Operate” attached to a control panel, a worker pulled the switch. That shut down the plant and the main transformer for southern Taiwan, triggering outages in that part of the island. Apparently, this wasn’t the first time the power was disconnected at this same location. In Bloomberg’s reporting of the story, it noted, “A technician’s error previously shut down the same plant in Kaohsiung last year, resulting in outages across Taiwan’s industrial parks.”

The latest weekly narrative from jobless claims was the farthest thing from cascading failures, storms or equipment meltdowns – it was a giant nothing burger. The effective unchanged, from 214,000 to 213,000, kept claims in an upward channel. Continuing claims remained range-bound at 1.85 million, neither improving nor deteriorating from recent levels; the current number was seen as far back as the middle of 2024. But as Thursday’s Feather explained, continuing claims now cover just 25% of the total unemployed population. As it skirts a record low, continuing claims’ efficacy as a labor gauge is increasingly challenged as an indication for the jobless narrative.

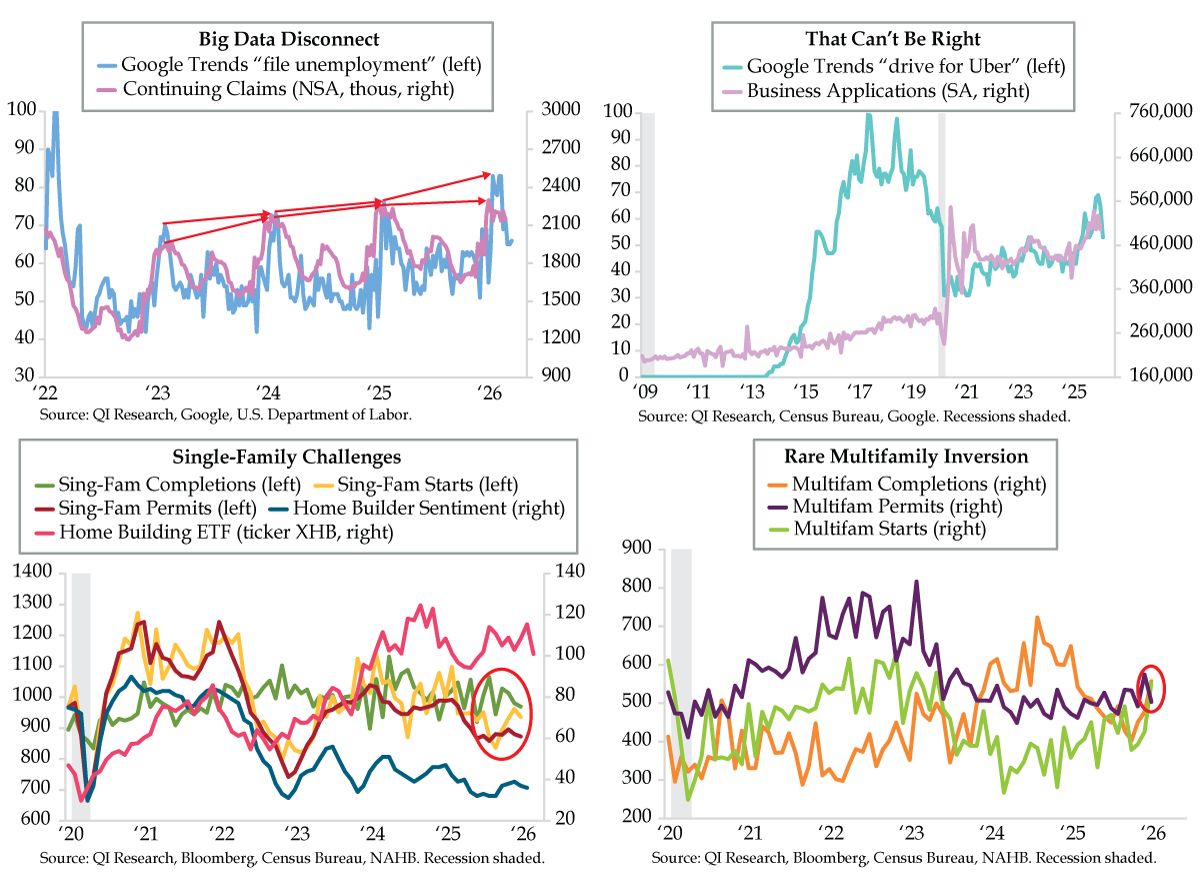

When questions like this arise, a look toward alternative data is appropriate. The latest update from Google Trends “file unemployment” search interest (lilac line) shows the big data series has detached from raw, not seasonally adjusted (NSA) continuing claims (light blue line). Seasonal patterns have shown that both series peak early in the calendar. The path from 2025 to 2026, however, portrayed Google’s higher propensity to file unemployment and the Department of Labor’s sideways pattern for continuing claims (diverging red arrows). Notably, the scorecard measured in year-over-year (YoY) rates thus far in 2026 shows an average gain for “file unemployment” of 11.3% compared to year-ago levels and a slight decline on average for continuing claims of -0.6% YoY. As the Google series is higher beta version, the disconnect is distinct.

We’ve explained in past analyses that the option for out-of-work individuals to drive for rideshare firms is a more profitable choice vis-à-vis being on the dole. That said, querying Google Trends with the phrase “drive for Uber” yielded results that puzzled and surprised us at the same time. Before diving in, Uber was founded in 2009, but it wasn’t until 2017 that search interest peaked. Following the pandemic, driving for Uber has been trending unevenly higher off the lows. After April 2025’s tariff terror, things picked up to 49 from March’s 43. Search interest did not peak until January’s 69 reading (aqua line).

Based on this sampling, opting for Uber appears to have gained traction relative to collecting unemployment. The puzzling outgrowth of this analysis is that the path of the Google Trends series neatly parallels that of the Census Bureau’s Business Applications (BA). The up channel in this gauge from January 2025’s interim low of 385,618 to the November 2025 high of 537,266 eased back to 496,443 by February 2026 (lavender line). Without “throwing the spaghetti” together on one graphic, the Business Applications series in isolation implies a superficial sign of economic strength. However, could this alternatively reflect entrepreneurial optimism driven (pun intended) by displaced workers making ends meet? In choosing to drive and form their own business, they thus apply “for an Employer Identification Number (EIN) on the IRS Form SS-4,” according to the BA report.

Shifting gears, Thursday’s economic calendar also brought a Census Bureau update from the new residential construction space. January housing starts came in well above expectations, rising 7.2% over the month to 1.487 million (vs. 1.341 million consensus). Building permits, however, disappointed and fell by 5.4% compared to December, to 1.376 million (vs 1.410 million consensus). The divergence was tied to the volatile multifamily sector. The larger single-family space continued to atrophy.

Single-family permits edged lower to an 873,000 rate (red line), farther below the 935,000 starts figure (yellow line) and nearly 100,000 under the 970,000 registered for one-unit completions (green line). Slippage in single-family home building mirror-images home builder pessimism. Recall, the National Association of Home Builders’ single-family sentiment survey started a quintuple dip this year, falling to 36 in February from the December 2025 interim high of 39 (dark blue line). The ongoing slump in the official single-family home building statistics is a key influence that’s kept the State Street S&P Homebuilders ETF (ticker XHB) from reattaining its September 2024 high; its two attempts — in August 2025 and in February 2026 – have both failed (fuchsia line).

As for developments in the multifamily complex, they sported a rare inversion in January. At 503,000, permits (purple line) ran below both starts, at 552,000 (lime line), and completions, at 557,000 (orange line). In overlapping history since 1968, there have only been 50 other instances out of 696 months when this upside-down situation has occurred, which guides for a downside correction as soon as next month. To that end, multifamily permits were 49,000 under starts. Following negative permits-starts spreads between 0 and -50,000, starts posted an 11% monthly decline the next month. The combination of negative technicals with fundamental pressures on the single-family side suggests a switch could be pulled next month. Sustained good news on housing starts is not in the offing.