Bachman-Turner Overdrive’s “You Ain’t Seen Nothin’ Yet” is an extraordinary case of an inside joke accidentally becoming a global anthem. In 1974, Randy Bachman recorded the track as a “work song” to test studio dynamics; it was never intended for public consumption. Because Bachman didn’t think it would be released, the band didn’t bother perfecting it – or even tuning their instruments. The famous “B-B-B-Baby” delivery was a lighthearted parody of his brother, Gary Bachman, who struggled with a persistent stutter; it was recorded as a gag for Randy to send Gary as a gift. When the band was finishing the Not Fragile album, their boss at Mercury Records, Charlie Fach, felt it lacked a radio-friendly hook. When Fach heard the song, he loved it, warts and all. In a Songfacts interview Bachman explained: “Charlie said, ‘I want to put this on the album.’ And I said, ‘I need to remix it.’ And he said, ‘Don’t touch it. Put it on the way it is. When you play this with the other songs, it just jumps off the turntable.’” The hit climbed to No. 1 in more than 20 countries.

Yesterday, a QI Pro inspired today’s “You Ain’t Seen Nothin’ Yet” top with this post in our Bloomberg chatroom: “Struggling to ignore the potential cost-push tsunami coming our way because of this conflict. Now if it all goes away, we can play the transitory game again. I get it. (But it) makes it very difficult to forecast, impossible, at least for me. But admittedly, I don’t spend much time on the survey calcs. But we are on the cusp of something potentially nasty, so it seems.”

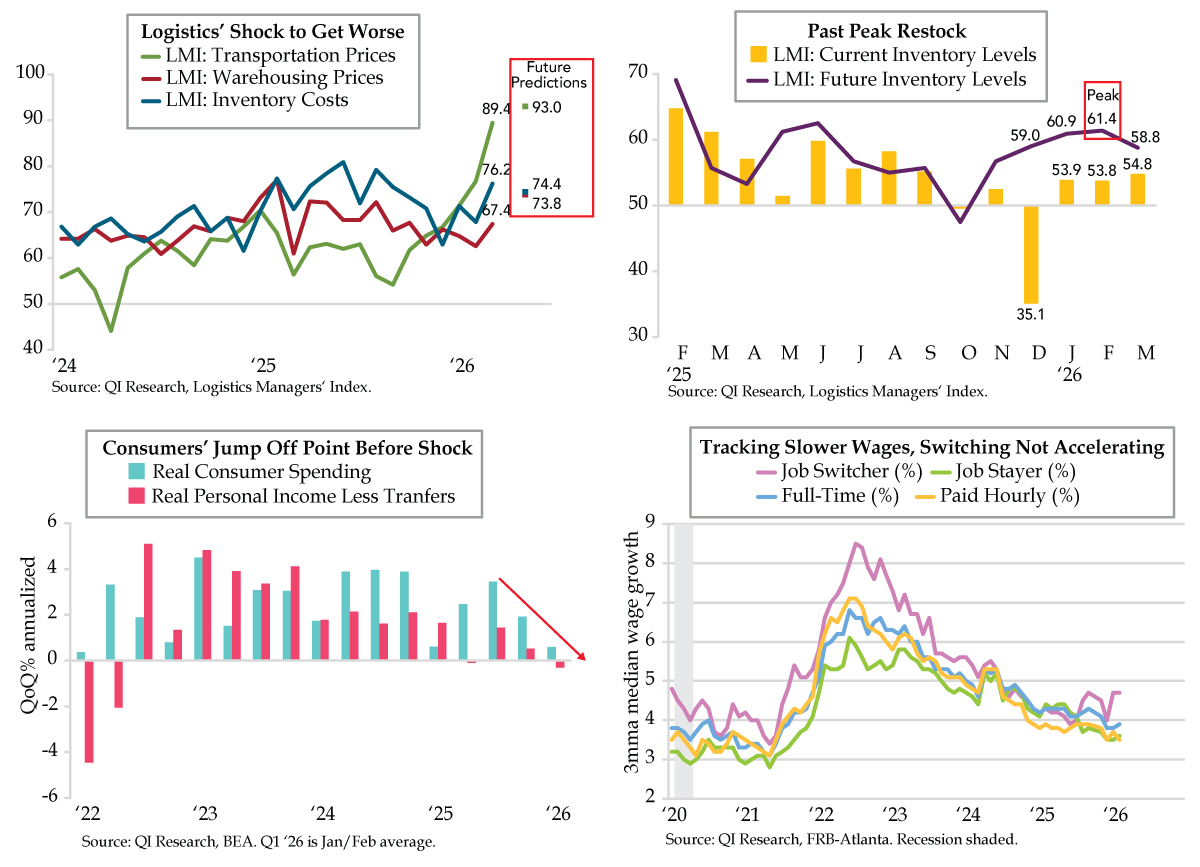

The Logistics Managers’ Index (LMI) agrees. Respondents to the March report indicated accelerating pricing across all three logistics categories of transportation, warehousing and inventories. The Transportation Prices index rose to 89.4 (green line), the highest since March 2022 when the Russia/Ukraine conflict pushed pricing to 89.7. Today’s shock is being felt throughout the supply chain as upstream (89.9) and downstream (89.6) show nearly identical readings. Pressure built up dramatically as the month unfolded: first-half March at 81.9 gave way to second-half March at 94.0. LMI’s future predictions for Transportation Prices at 93.0 don’t show any let-up, whether of the upstream (93.4) or downstream (91.7) variety.

Warehousing Prices also jumped in March, increasing 4.8 points to 67.4 (red line). Here, too, upstream (67.5) and downstream (67.4) were virtually identical, and the month ended with greater momentum (at 70.2 in second-half March) vis-à-vis the first two weeks after the Iran War began (at 63.2 in first-half March). Future pricing advanced to 73.8 with upstream (77.0) anticipating a bigger cost hit than downstream (65.2).

And finally, Inventory Costs posted a significant 8.4-point increase to 76.2 (dark blue line). Downstream (87.5) was markedly higher than the upstream figure (71.6). From early to late March cost pressures were elevated and steadily moved from respective levels of 77.3 to 77.5. The LMI noted that in both cases, “the cost numbers are roughly 20 points higher than the inventory level numbers. The outlook points to significant cost increases at 74.4 over the next 12 months, more so upstream (77.6) than downstream (66.7).”

All three of these logistics’ costs pose an inflationary risk that threatens to be passed down to end consumers. LMI aggregated Transportation, Warehousing and Inventories on a current and future basis concluding: “On aggregate, the three cost/price metrics come in at 241.2. In the past, logistics cost expansion at that level was a forerunner of robust supply-driven inflation. If these predictions hold, it is possible that inflation will once again become an issue, which in turn could actually drive logistics demand back down.” In the business, we call that a “cliff effect.”

A few months back, when LMI’s Inventory Levels sunk to December’s 35.1, we became bullish on the Transports sector. Now, demand destruction for the restock narrative is a clear threat. And it appears to be happening at smaller companies. This LMI excerpt illustrates: “What is surprising is how much small firms said costs increased, at 72.0, when they said Inventory Levels were exactly flat, at 50.0. This means nearly three-quarters of small firms said costs increased, even when levels did not.”

We are past peak restock, with Future Inventory Levels easing from February’s 61.4 to March’s 58.8 (purple line); that’s nearly the same as December, when Current Inventory Levels collapsed to 35.1. More importantly, a full normalization should have been represented by at least one month of the Current measure, about 15 points above the breakeven 50-line, to match the December compression. But that hasn’t happened as March’s print was just a 54.8 print (yellow bars).

Even if higher costs need to be passed down to the consumer, can they be? From a downstream demand perspective, the U.S. consumer sector’s jump-off point before the Iran War/Oil/Logistics’ Shock showed both slower spending and income momentum in 2026’s first quarter. Defaulting to two varsity NBER recession indicators, real consumer spending was up a mere 0.6% on a quarter-over-quarter (QoQ) annualized basis, down from 3.5% and 1.9% in 2025’s third and fourth quarters, respectively (aqua bars). Households’ source for purchasing power — current income — looks even worse. Real personal income less transfers fell 0.3% QoQ annualized over the first two months of 2026’s first quarter, down from gains of 1.4% and 0.5% in the previous two periods (fuchsia bars).

Both March and April spending and income should face notable downdrafts once adjusted for inflation. Should the first quarter end on weak footing and the second quarter therefore start off in weak fashion, quarterly arithmetic will make it very difficult to see things in the black for either NBER gauge. Wage pressures, as depicted through the Atlanta Fed’s Wage Growth Tracker, pile on and show slackening paths for full-timers (light blue line), hourly workers (yellow line) and job stayers (lime line). Even the lack of acceleration in wage growth for job switchers (lilac line) suggests the money-grab factor has waned amidst rising job insecurity. Randy Bachman would concur that “You ain’t seen nothin’ yet.”