If it’s a remote paradise you seek, Mystery Island should be on the list. Located at the southernmost tip of the Vanuatu archipelago in the South Pacific Ocean, Mystery has no permanent residents, electricity, running water, hotels or infrastructure. Why go? Perhaps because it’s surrounded by a perfectly protected, crystal-clear marine sanctuary teeming with coral reefs, sea turtles, and clownfish. Little wonder it’s a premier port of call for cruise ships sailing out of Australia. Passengers invade the pristine white beaches to snorkel, kayak and swim in its turquoise water. But by 3:00 pm, an “evacuation” order is given. Owned by the indigenous people of Aneityum, local custom dictates that Mystery Island is strictly a daytime destination. The Aneityumese believe the islet is haunted by spirits after dark, so they refuse to sleep there. Mystery Island is deserted every night, when it returns to absolute, eerie silence, left entirely to ocean breezes.

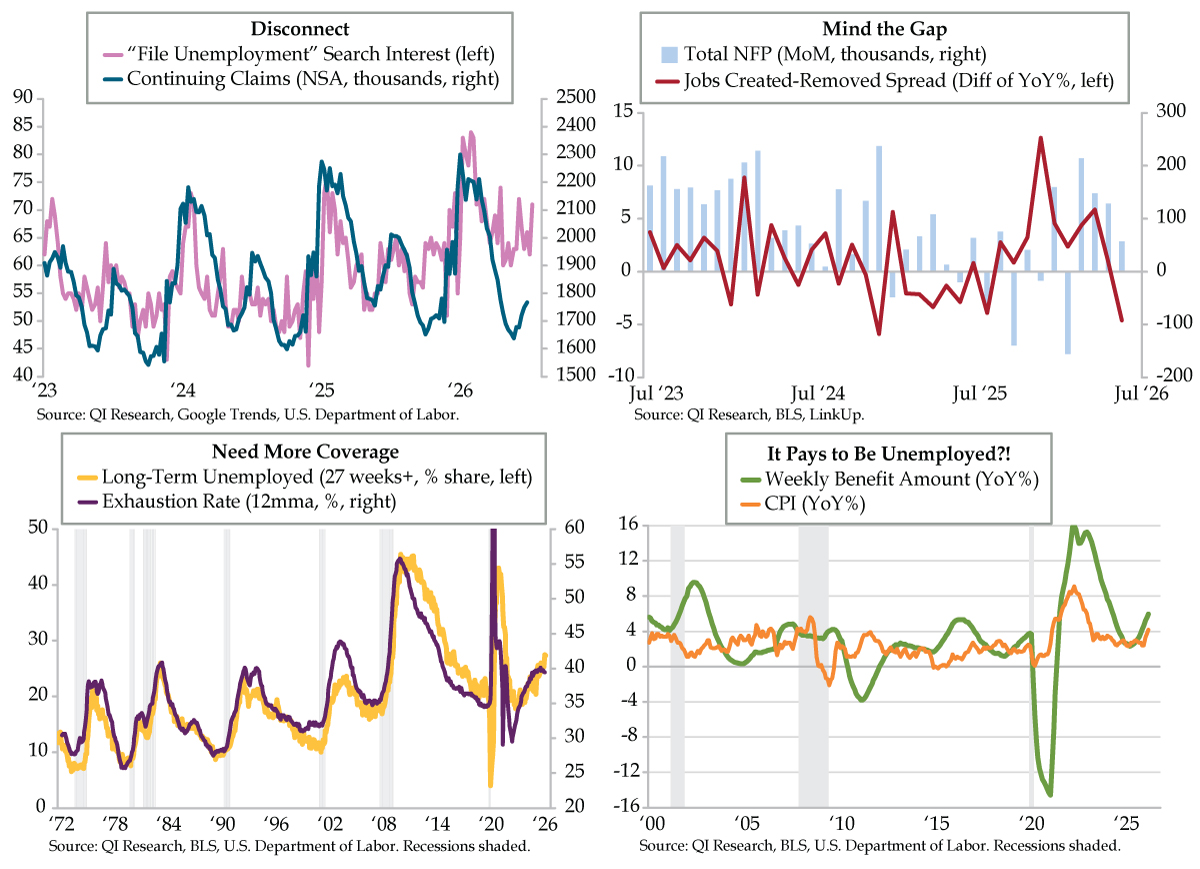

The U.S. labor market offers a disconnect resembling no island paradise. Exhibit A pits continuing claims (dark blue line) against big data from Google Trends (lilac line). Over the last few years, weekly oscillations in the not seasonally adjusted (NSA) subset of total unemployment have been flagged by “file unemployment” search interest. Regular winter/summer peaks and spring/autumn valleys for both metrics were drawn in a similar fashion. This year started the same way…until the disconnect began in late-March. Seasonal lows were staked in May for each series, but a distinct difference was drawn: a higher low for Google Trends and a lower low for continuing claims.

Leaving that puzzle in the rear-view mirror, LinkUp’s Monthly Jobs Recap gave a straightforward headline from its dataset via the top 10,000 global employers: “U.S. Hiring Remains Subdued as Job Listings Continue to Soften.” Because job postings are perpetually created and removed dynamically, the spread between these measures guides the direction of employment growth. In June, LinkUp indicated that 1,634,124 jobs were created via-a-vis the 1,787,063 removed. Since the survey’s 2012 inception, the -152,939 inversion was the second worst behind November 2022’s -153,093. June 2026 was also the worst June on record.

Since the LinkUp data are reported on an NSA basis, year-over-year (YoY) comparisons best normalize – and seasonally adjusting – comparisons. It’s here where the Jobs Created-Removed spread earns its stripes. Taking the difference between YoY rates, the recent pattern points to a further softening in nonfarm payroll job growth. Creating listings postings rose 17.4% YoY in June, 4.6 points less (red line) than the Removed listings’ 22.4% YoY figure. Cost-cutting anew is the fundamental read when this guide has traveled from December’s local high of 12.6 into the red. To be sure, the runup to that point and drop off since foreshadowed slowing NFP. Farther back, the persistent negative spread in late-2024/early-2025 flagged the NFP declines in 2025’s second half. For good measure, the last time the spread was this deeply inverted (December 2024’s -5.9), NFP posted an outright contraction the very next month.

Given the downside risk for the August 7th Employment report, incorporating the forensics on long-term unemployment is apropos.Given the downside risk for the August 7th Employment report, incorporating the forensics on long-term unemployment is apropos. The share of unemployed 27 weeks and over pushed through the 27%-level in May and June; it’s been on the upswing since reaching May 2025’s 20.4% interim low (yellow line). As the bankruptcy cycle continues apace, long-term unemployment has advanced on a YoY basis for 31 consecutive months, a streak last seen during the Great Recession.

Resultant permanent scarring still climbing, this development is historically met by greater ranks of jobless benefit receivers exhausting their benefits. That means they’ve been receiving them in the first place. Herein lies a conflict. The exhaustion rates’ 12-month moving average is showing signs of cresting from November’s 40.1% to May’s 39.5% (purple line). Both figures move cyclically over time. The divergence suggests more coverage is needed for those not covered by regular state benefits that run out after 26 weeks. According to the U.S. Department of Labor, average duration in the regular program hit a cycle high 15.75 weeks in May. This lengthening reinforces the effect of scarring and the need for more coverage.

In an ironic twist, we ask, does it pay to be unemployed? Average weekly benefit checks are growing faster than inflation. In May, weekly benefits rose 5.9% YoY (green line), outpacing the CPI’s 4.2% YoY rate (orange line). Prior to the pandemic’s massive volatility, the last time benefits grew at this rate was March 2003, at 6.1% YoY. By no means do these transfer payments dictate consumer spending — over time, they’ve accounted for a smaller share of take-home pay. For those “fortunate” enough to receive higher-paying benefits, the truth is they only cover about one-third of disposable income.

Higher long-term unemployment and the jobless risks depicted by LinkUp’s have combined to keep purchasing power on its heels. If Revelio’s June tally of WARN notices is accurate, there may be a temporary reprieve. In its July 1 release, it noted that 17,637 workers were notified that their jobs were in jeopardy, the lowest since December’s 17,323. This detail suggests that the easing in initial claims from the June 6th 230,000 local high to the July 4th 215,000 level may not be complete.

The relatively better WARN data present a test for jobless claims in coming weeks. A fall back near the 200,000-level ahead of the July 29th FOMC confab could validate the minority that entertained a June hike. With oil also stopping its fall on Iran-U.S. tension, inflation risks could outweigh unemployment worries rendering the 24% and 75% rate hike probabilities for July and September too low. Conversely, earnings season is upon us. Should Corporate America choose to use the margin damage exacted by the Iran War as another excuse to cut costs, the layoff reprieve could prove to disappear as abruptly as tourists on Mystery Island after 3:00 pm.