Unfriend (verb): To remove someone as a ‘friend’ on a social networking site such as Facebook.

The word became so prominent after its social media adaptation that Oxford University Press named “unfriend” its 2009 Word of the Year. Christine Lindberg, Senior Lexicographer for Oxford’s U.S. dictionary program explained: “It has both currency and potential longevity. In the online social networking context, its meaning is understood, so its adoption as a modern verb form makes this an interesting choice for Word of the Year…it assumes a verb sense of ‘friend’ that is really not used (at least not since maybe the 17th century!). Unfriend has real lex-appeal.” Dad jokes aside, English scholar, preacher and author Thomas Fuller is credited with its usage in a 1659 letter: “I Hope, Sir, that we are not mutually Un-friended by this Difference which hath happened betwixt us.” But “unfriend” was used even earlier, as William Shakespeare demonstrated in 1602’s Twelfth Night: “Being skilless in these parts; which to a stranger, unguided and unfriended, often prove rough and unhospitable.”

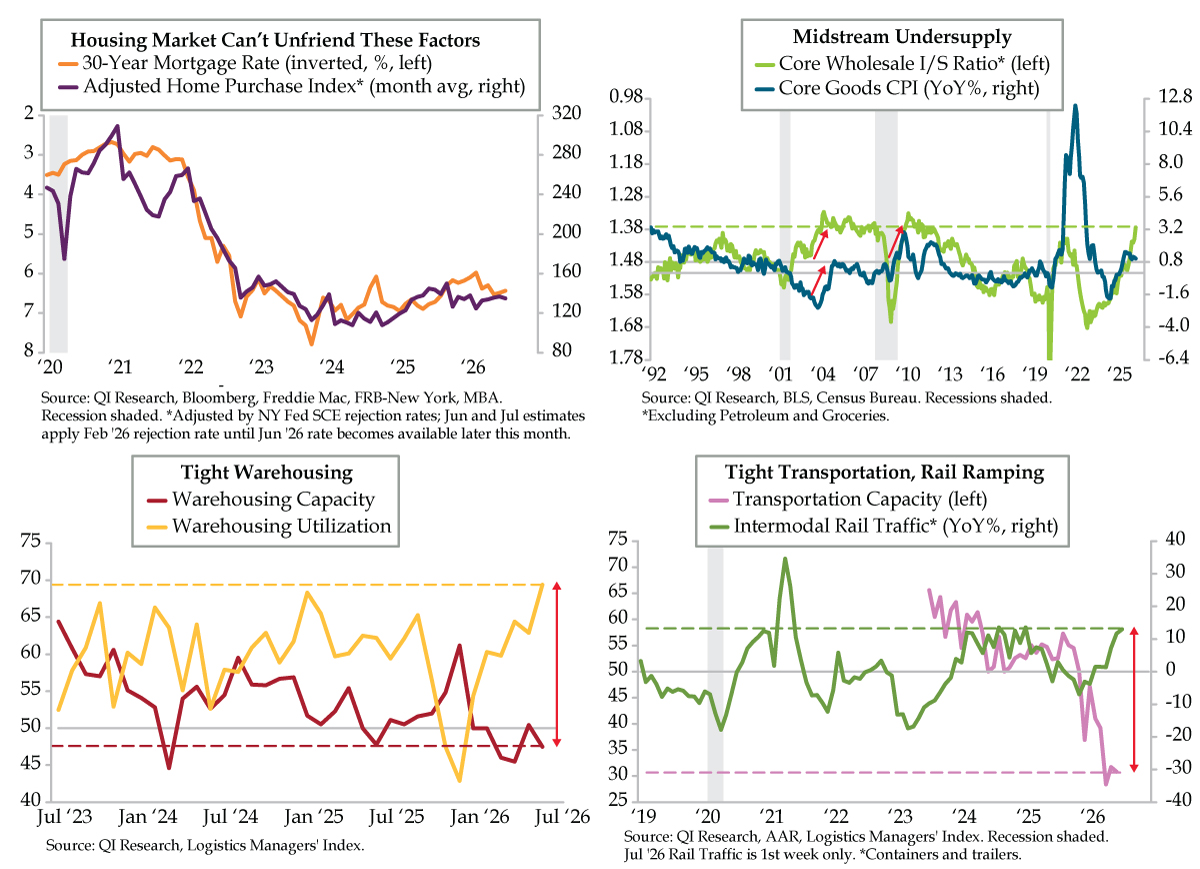

The U.S. housing market would love to unfriend high mortgage rates. After peaking close to 8% in late 2023, the Freddie Mac 30-year rate has meandered between 6% and 7%; it’s currently at still-too-high 6.43% (inverted orange line). As such, since topping in the week ended January 16th at 194.10, the Mortgage Bankers’ Association (MBA) Purchase Index has flatlined. The 169.50 level in the week ended July 3rd sits atop its year-to-date average where it’s been since mid-June.

MBA’s mortgage application data is fallible when wages have round-tripped to 2019 levels – much of the “activity” tracked is double-counting. More importantly, mortgage apps are a snapshot in time and exclude cancellations, something home sellers would also like to unfriend. QI’s Adjusted Home Purchase Index reflects lender rejection rates as reported by the New York Federal Reserve’s Survey of Consumer Expectations Credit Access Survey; they’ve run north of 20% since last October. Helped by a gradual decline in mortgage rates, the Adjusted Index peaked in September 2025. At the time, the year-over-year (YoY) trend was expanding at a 24.4% rate. Contrast that with July 2026 — the preliminary 6.1% YoY drop is 2026’s worst showing marking a fifth straight YoY decline.

Getting the housing market back on its feet is not on the Fed’s To-Do list. Price stability is the primary goal as reiterated in yesterday’s FOMC minutes, which revealed a few participants believed there was a case to raise rates in June.

May’s Wholesale Trade report satisfied hawks’ appetite. June’s Core Wholesale Inventory/Sales ratio fell to 1.374, the lowest number since April 2011 (inverted lime line). The midstream supply-demand excludes food (i.e., groceries) and energy (i.e., petroleum products) allowing for an apples-to-apples translation to the consumer price (CPI) picture. Two previous episodes in the early 2000s expansion and the 2007-09 recession test-case today’s backdrop. The decline to April 2004’s low of 1.327 was a harbinger of Core Goods CPI inflation reaching escape velocity to exit deflation in late-2004 which had been in place since the economy exited the 2001 recession. And the sustained and sharp drop in the Core Inventory/Sales ratio from the January 2009 cycle high of 1.663 recovery culminated with a Core Goods inflation acceleration from -0.5% YoY to 3.0% by 2009’s end.

While wholesale pressures can continue to be eaten by margins, and not fully passed through to strapped consumers, Fed policymakers will likely remain cautious. The Logistics Managers’ Index (LMI) stands as further validation. Warehousing Capacity fell to 47.5 in June (red line), the fifth time in the last three years under the 50-breakeven-line; notably; three hit in the last four months.

The report offered one reason for the busyness: “Tariffs may increase later in July, so some of what we’re seeing is a pull-forward ahead of peak season.” Warehousing Utilization rose 6.5 points to 69.4, the highest since September 2022 (yellow line), evidence of the impulse to source product as trade policy uncertainty collides with real-world inflation expectations. The Utilization-Capacity spread was more pronounced for large firms (72.9-50.0=22.9) than their small counterparts (66.7-45.7=21.0). That stands to reason as the former are price leaders; theoretically, they’ve got more pricing power.

Elsewhere, Transportation Capacity fell nearly a point to June’s 30.8 (lilac line). The LMI acknowledged the sudden swing: “Transportation Capacity has now read in below 40.0 for four consecutive months – a streak that came after 51 straight months above that number.” QI has described the trucking cost burdens and supply-side tightness in previous commentaries. The LMI went on to explain that “the increase in Transportation Prices was significantly accelerated by oil prices, but they are staying up now because of the dearth of Transportation Capacity. A byproduct of these dynamics is a shift towards rail…the surge in activity has slowed throughput for the big four U.S. railroads, with all of them reporting recent lows in intermodal train speeds.” Intermodal traffic has accelerated to a 12.9% YoY rate thus far in July (green line), the biggest since January 2025. Railroads are clearly not in the business of unfriending tightening logistics.

The question, which all Fed policymakers are actively avoiding, is how to square wage disinflation. In its July Freight Market Update, C.H. Robinson laid out the dilemma: “Retailers are increasingly competing for a limited pool of consumer spending by concentrating promotions into shorter periods. While the strategy can boost traffic and sales, it also creates significant strain on inventory planning, fulfillment operations, and transportation networks.” Suffice it to say, institutionalizing uncertainty will not bode well for the labor market or procurement specialists anxious to plan rather than swing with the vagaries of impulsiveness. If nothing else, rails will continue to benefit by force.