“Survive we did, but it was close. Our mission was a failure, but I like to think it was a successful failure. Apollo 13, scheduled to be the third lunar landing, was launched at 1313 Houston time on Saturday, April 11, 1970; I had never felt more confident…Looking back, I realize I should have been alerted by several omens that occurred in the final stages of the Apollo 13 preparation…. Oxygen tank No. 2 blew up, causing No. 1 tank also to fail. We came to the slow conclusion that our normal supply of electricity, light, and water was lost, and we were about 200,000 miles from Earth. We did not even have power to gimbal the engine so we could begin an immediate return to Earth. The message came in the form of a sharp bang and vibration. Jack Swigert saw a warning light that accompanied the bang, and said, ‘Houston, we’ve had a problem here.’” – Apollo Expeditions to the Moon, James A. Lovell

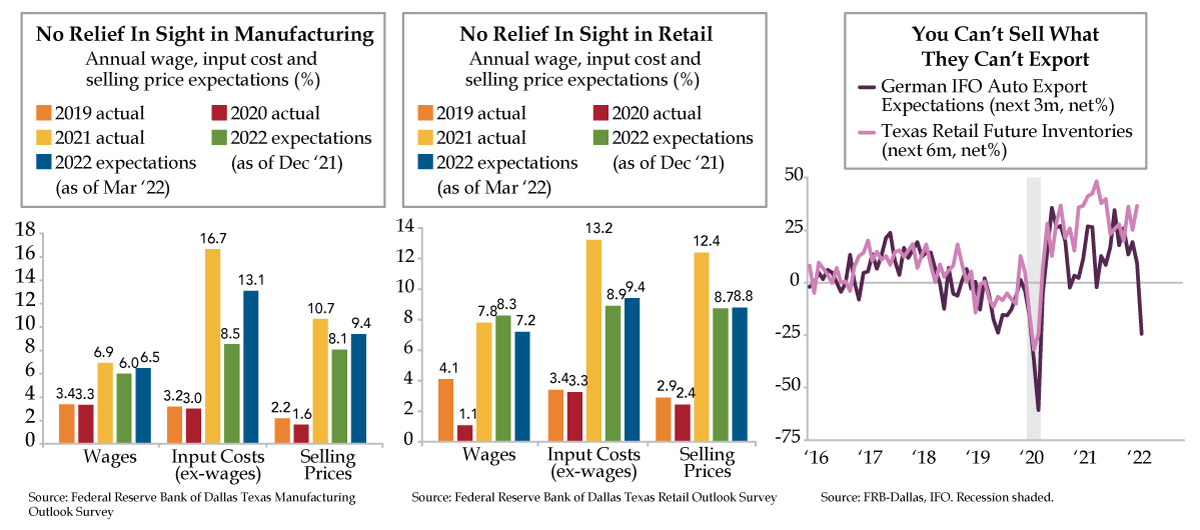

For dramatic effect, 1995’s Apollo 13’s screenwriter William Broyles Jr. changed the famous quote to, “Houston, we have a problem.” Today, Houston and the rest of the state of Texas, has a problem – verb present tense. It’s that inflation has got everyone on alert for the dreaded wage/cost-to-price spiral. The Dallas Federal Reserve’s March business outlook surveys illustrated the anxiety via special supplemental questions. Today’s twin bar charts reveal the emergence of persistent inflation from the beginning of the production process to the end of the distribution chain.

In manufacturing, annual wage costs in 2021 and expected in 2022 are running at nearly double that of 2019 and 2020. Input costs (excluding wages) have accelerated more quickly as supply chain disruptions continue to constrain roughly three-in-four Texas producers. Price adjustments have quickened to five times the pre-pandemic rate. The follow-through from selling prices suggests a wage/cost-to-price spiral is unfolding.

There’s a similar picture in retail. Wages are expanding at a 7% annual clip while those net of wages vaulted to 13% last year; they’ve since fallen back to around 9%. The resultant rising consumer prices speak to the Fed’s challenge to get inflation back to its 2% target. Retail inflation of 2.5% to 3% in 2019 and 2020 vaulted over 12% in 2021, but also has settled near 9% in 2022. The absolute level is still running three times too hot even as discretionary wherewithal is crumbling.

When queried, “what is the net impact of recent higher energy prices on your business?” 74% of Texas retailers saw a slight to significant impact, while only 5% indicated positive effects. Expanding further, Lone Star state retailers were asked what the net impact of the Russia-Ukraine war was on their business, 31% answered negatively, while again just 5% leaned positively (we’d like to meet that 5% that found war to be a boost).

Our praise for Texas as a key manufacturing hub has been a constant over the years – the vista from our Dallas HQ provides a convenient vista. For all of the details we’ve shared over the years, we share for the first time that more than eight cents of every dollar American expended is within its borders. For the key cyclical auto sector, the footprint is even bigger. According to the Texas Department of Motor Vehicles, there are more than 2,500 licensed new (franchise) vehicle dealers across the state. All told, Texas accounted for 11% of 2020’s new vehicle spending, eclipsing the larger state of California for the second year in a row.

To take but one example from Rodeo Drive, Dallas is the Maclaren capital of the country. It’s true…there are more than big pickup trucks down here. There is a booming import car market as well, which brings us to last Friday’s German IFO survey, which slammed estimates. The war in Ukraine drove a record decline in business expectations across the German economy. To diverge from our theme for just a moment, unlike during the trade war days when it was a standout economic diversifier, construction expectations also got shellacked.

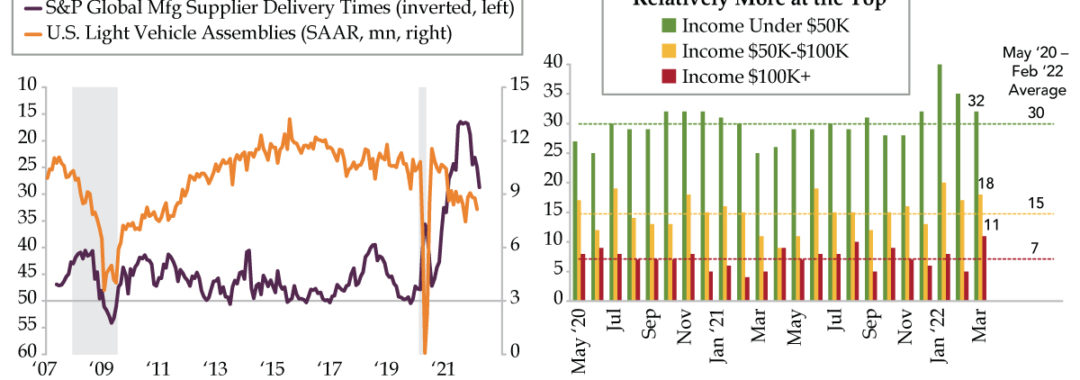

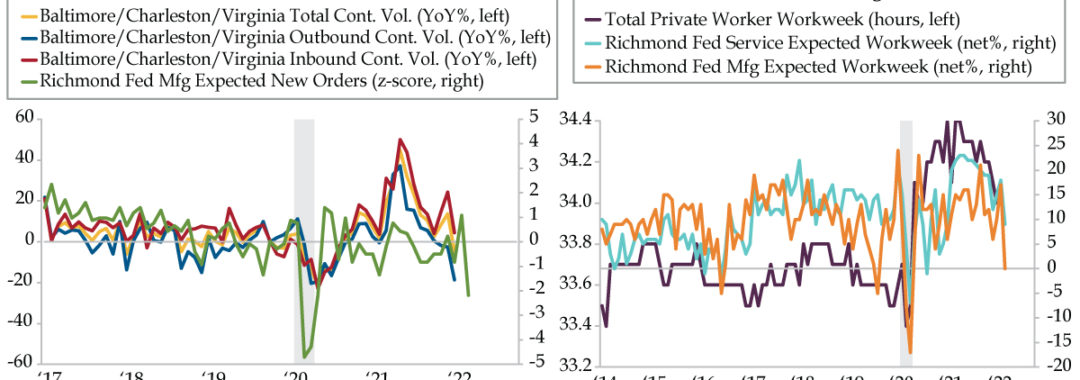

As for manufacturing, at -40.5, the net difference was also worse than IFO’s headline; the motor vehicle industry got hit even harder with a one-month swing a nasty -57.5 points. It’s little wonder German auto export expectations plummeted in March (purple line). Texas’s mammoth auto dealer footprint naturally makes it sensitive to the ups and downs of Germany’s Big Three brands — BMW, Daimler, and Volkswagen. To that end, Texas retail future inventories (orange line) have had a .67 correlation since 2016.

Rising auto loan rates will only act as an additional governor on new car sales. In this year’s first quarter, Bankrate’s 60-month new auto loan in Texas has already skipped up by a half a percentage point. A follow through on the Fed’s hiking cycle threats in coming months would hypothetically further pressure the top line even as employers continue to carry high labor costs. As you will hear with greater frequency, unemployment is the most lagging of all economic indicators; relief on this front won’t come soon enough to preserve margins.

On a more fundamental level, Texas auto dealers have a hard time selling what German automakers can’t export. Consensus estimates for Friday’s March vehicle sales point to a 13.9 million seasonally adjusted annual rate, down a smidge from February’s 14.1 million. We’ll take the under.