Reflex Thursday

Here’s Ben Stein in his best monotone explaining how reflexes work: “Polysynaptic spinal reflex arcs and brainstem-mediated neural pathways execute rapid involuntary motor responses that…

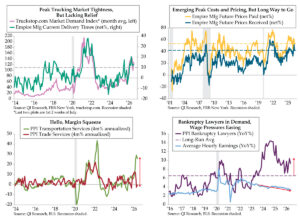

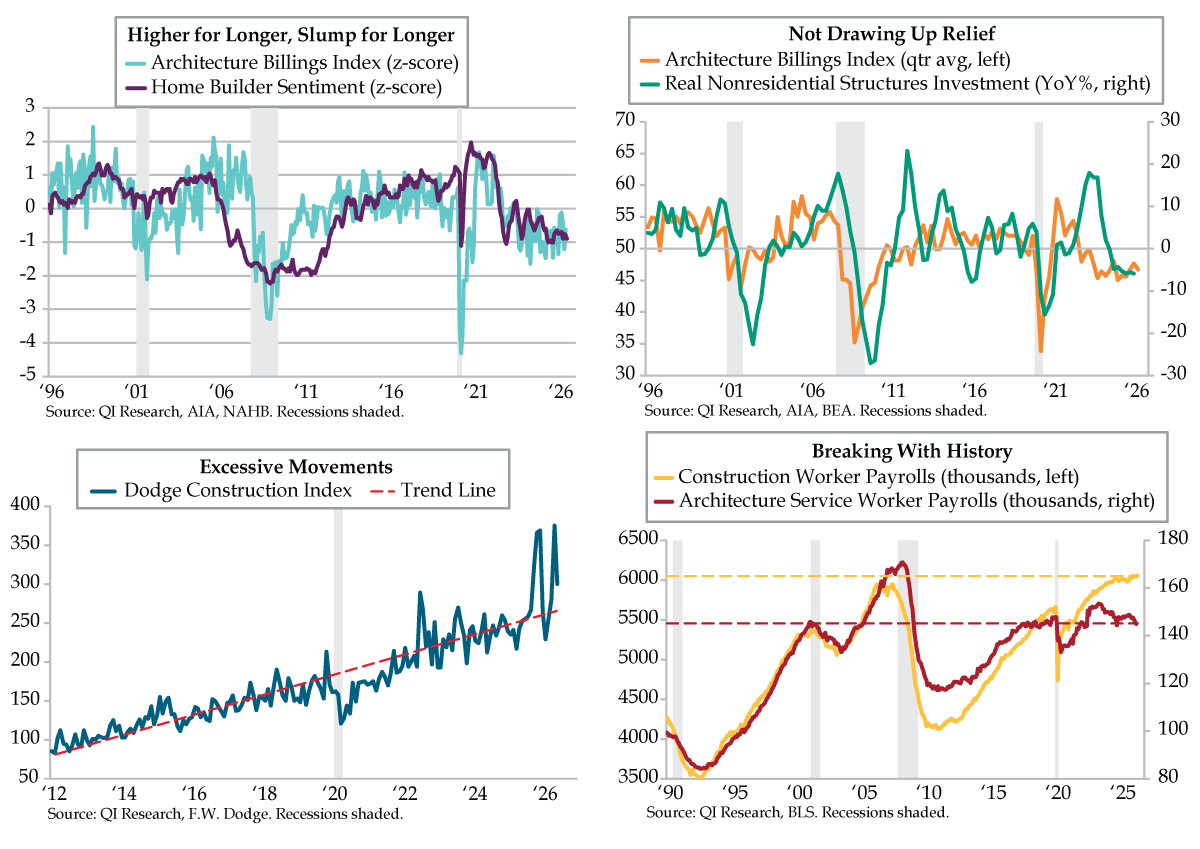

Of Baseball and Architecture Slumps

“Dave Campbell had a hitless streak in 1973 that spanned 45 at-bats. Although the entirety of the streak occurred in one season, his struggles remained…

World Cup Was No Operation Mincemeat

Few operations are as renowned as Operation Mincemeat. Conceived by British Intelligence to fool the Germans about the target for the Allied invasion, the Imperial…

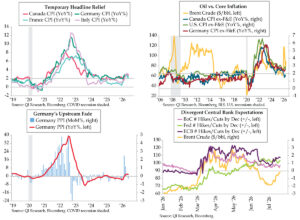

Inflation Headache Remedies

According to The Old Farmer’s Almanac, U.S. regional traditions have birthed many unconventional headache home remedies. Take Pennsylvania Dutch Powwowing. To cure a headache, a…

Cock-a-Doodle-Doo!

A vacation to Hawaii is guaranteed to have crystal blue waters, palm trees blowing in the wind, and pina coladas on tap. However, if you’re…

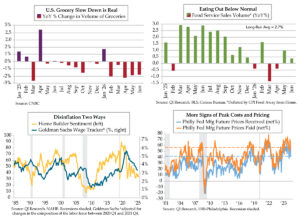

Food for Thought

And many a time beside their leafy bower The father sat, and heard, in silent joy, The youthful pair, in that most happy hour With…

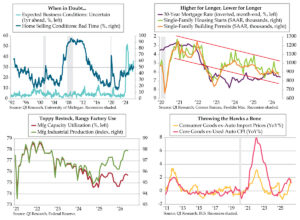

From Collar City to Margin Squeeze

Triumph of Excellence Wilbur’s Double Wear Trademark Points 2½ in. Highest Possible Grade 25 cents Quo Vadis Two Lives In One. No Wrong Side. The…

Inflation Eclipse Glasses

The next total solar eclipse lands on August 12, 2026. If these heavenly events are de rigueur in your world, pack your bags for Greenland,…

An Inflation Toast to Two French Revolutions

Commemorating the 1789 Storming of the Bastille, which launched the French Revolution, Bastille Day is celebrated every July 14th, and is, (bien sur!) a French…

Sticking Around

“People say that I am so controversial, but I think the most controversial thing that I have ever done is stick around.” One of…

Want to Disconnect? Try Mystery Island?

If it’s a remote paradise you seek, Mystery Island should be on the list. Located at the southernmost tip of the Vanuatu archipelago in the…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

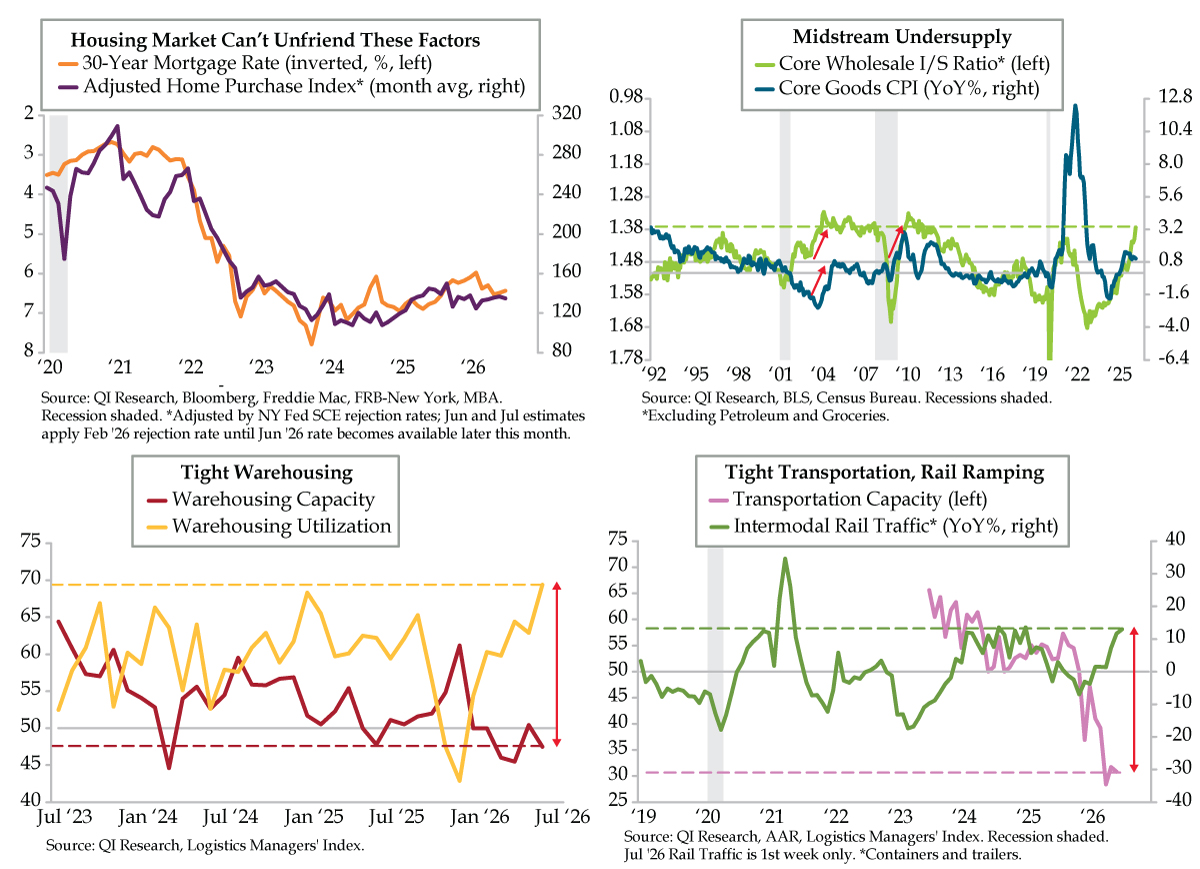

Unfriending Has a Long History

Unfriend (verb): To remove someone as a ‘friend’ on a social networking site such as Facebook. The word became so prominent after its social media…

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

122

123

124

125

126

127

128

129

130

131

132

133

134

135

136

137

138

139

140

141

142

143

144

145

146

147

148

149

150

151

152

153

154

155

156

157

158

159

160

161

162

163

164

165

166

167

168

169

170

171

172