Welcome to Major League Eating

Major League Eating (MLE) is the world body that oversees all professional eating contests. Even the casual observer is familiar with the MLE-sanctioned Nathan’s Famous…

The “Fixer”

“He/She will not do or commit anything tending to degrade him/her in society or bring him/her into public hatred, contempt, scorn or ridicule, or tending…

Don’t Mess with Rocky

Adrian: There's one thing I want you to do for me. Rocky: What? Adrian: Come here. Rocky: What? Adrian: Win, win... Mickey: What're we waiting…

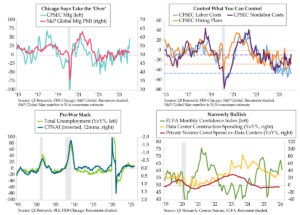

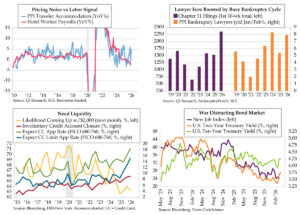

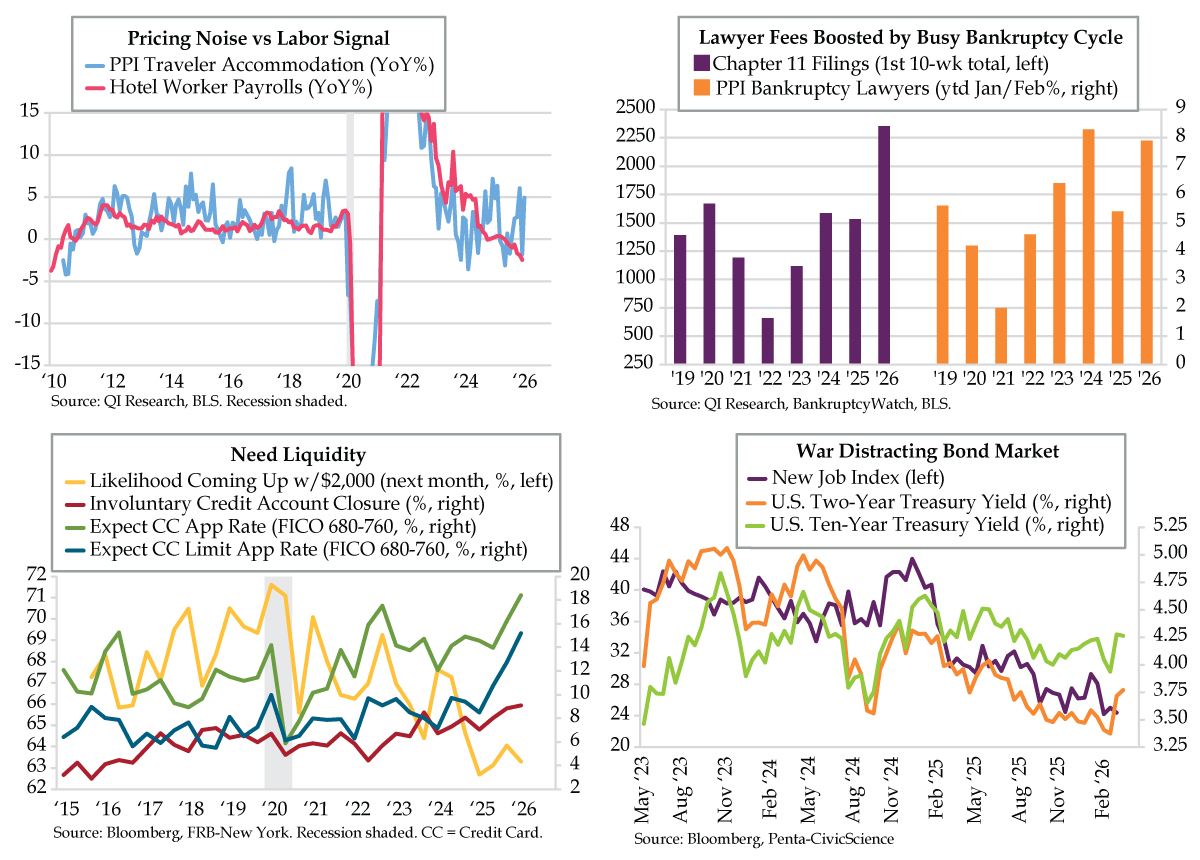

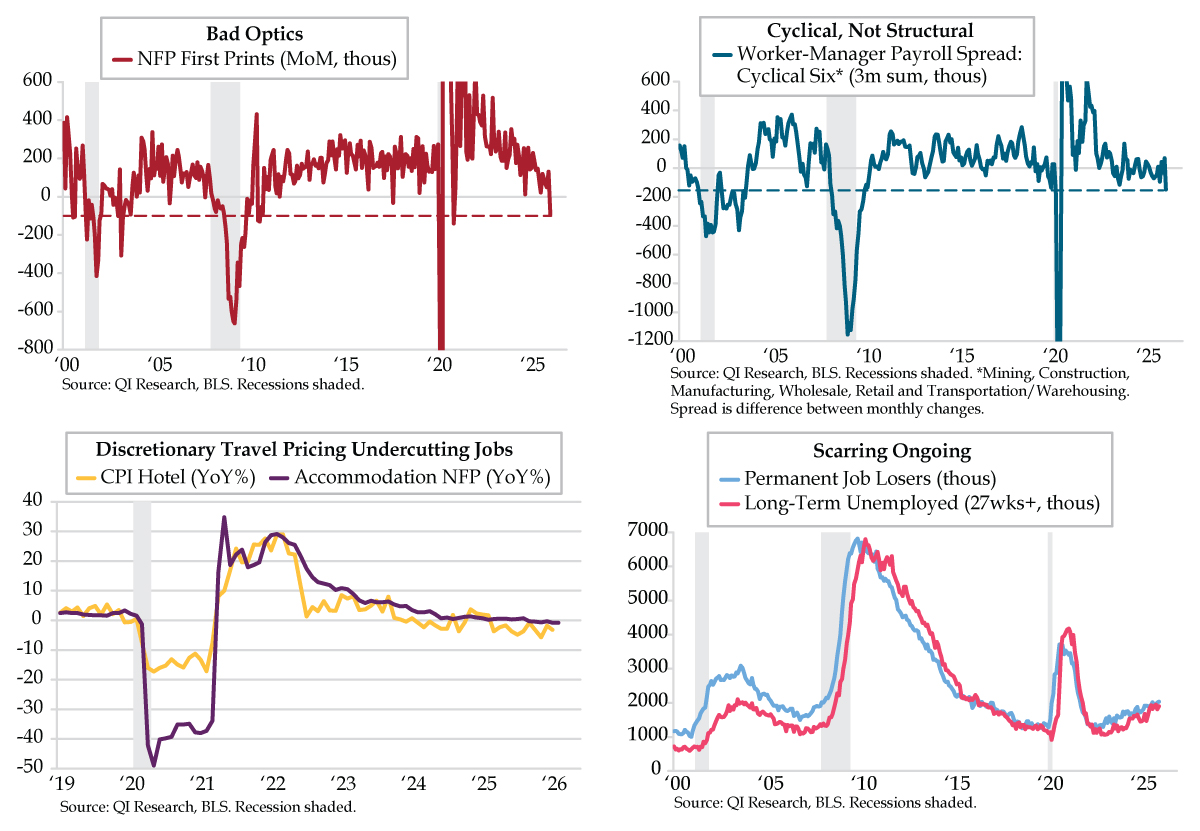

Pareidolia Spells No Fed Relief

If you think you’re seeing things, then you’re not alone. Pareidolia is the tendency for the human brain to see meaningful patterns or images in…

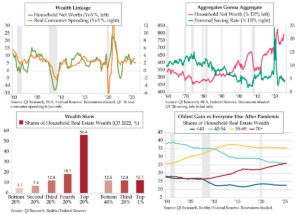

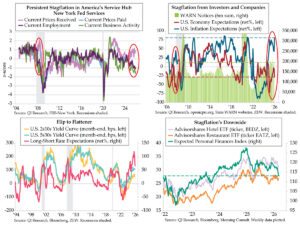

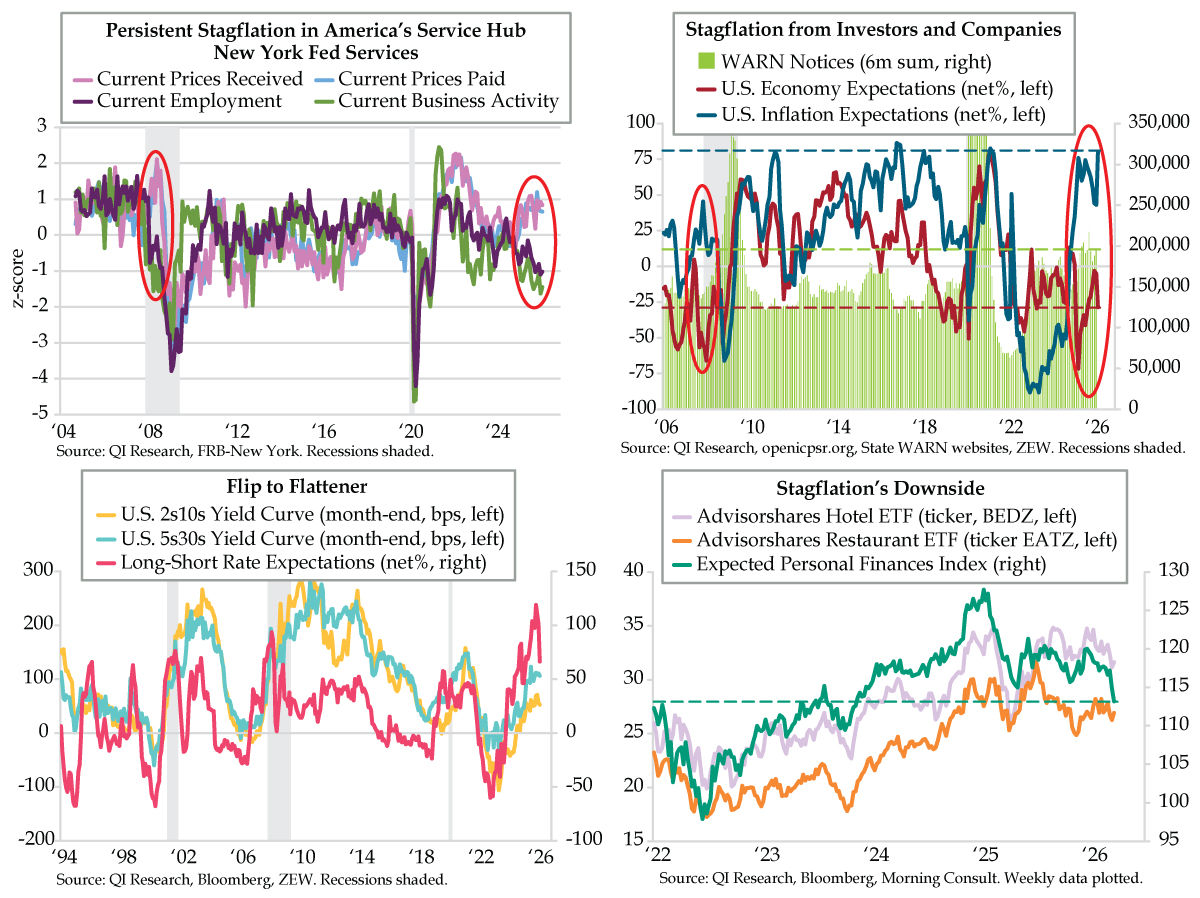

Stagflation: Worst of Both Worlds

“We now have the worst of both worlds – not just inflation on the one side or stagnation on the other, but both of them…

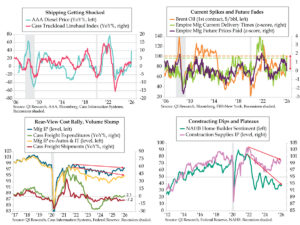

Shockers

U.S. colleges have the weirdest nicknames, like the UC Santa Cruz Banana Slugs, Delta State Fighting Okra and Presbyterian College Blue Hose, to name a…

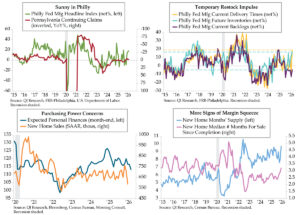

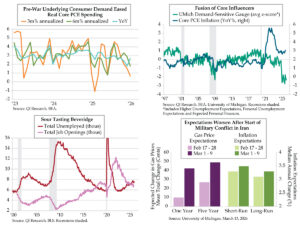

Light at the End of the Tunnel

“LIGHT AT THE END OF THE TUNNEL!” On April 6, 2020, President Trump tweeted this turn of phrase, expressing optimism that the COVID pandemic would…

Pulling the Switch

Most major blackouts are the result of cascading failures, storms or even equipment meltdowns, but there have been instances where human error caused a massive…

Cadillac Man

Larry: Tell them to stay back or I’ll blow this place and half the ****** block to hell. Joey: Stay back or he’s gonna blow…

Chomping at the Bit

“Chomping at the bit” originates from the high-tension-induced air at the starting gate of a horse race -- an equine so eager to run that…

Keep Calm and Carry On

“Keep Calm and Carry On” is an archetype lost and found story. Originally designed by the British Ministry of Information in the Summer 1939, it…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

An Unsolved Italian Murder

“I may be an unbeliever, but I am an unbeliever who has a nostalgia for a belief.” Pier Paolo Pasolini In 1975, Italian film…

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

122

123

124

125

126

127

128

129

130

131

132

133

134

135

136

137

138

139

140

141

142

143

144

145

146

147

148

149

150

151

152

153

154

155

156

157

158

159

160

161

162

163

164

165