The Feather — Charts of the Week

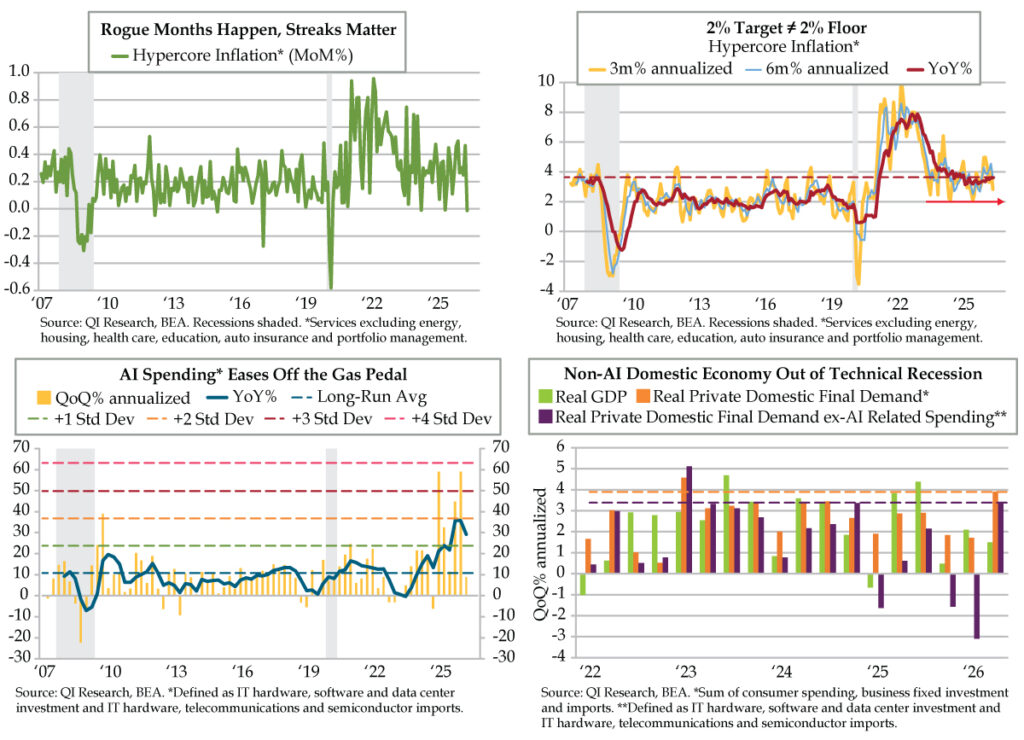

I’ve Fallen and I Can’t Get Up

Welcome to Quill Intelligence Please sign in or hit subscribe above. Thank you for visiting, The Quill Intelligence Team Username […]

The 23 Enigma

Welcome to Quill Intelligence Please sign in or hit subscribe above. Thank you for visiting, The Quill Intelligence Team Username […]

Echo Locations

Welcome to Quill Intelligence Please sign in or hit subscribe above. Thank you for visiting, The Quill Intelligence Team Username […]

For Your Eyes Only

Welcome to Quill Intelligence Please sign in or hit subscribe above. Thank you for visiting, The Quill Intelligence Team Username […]

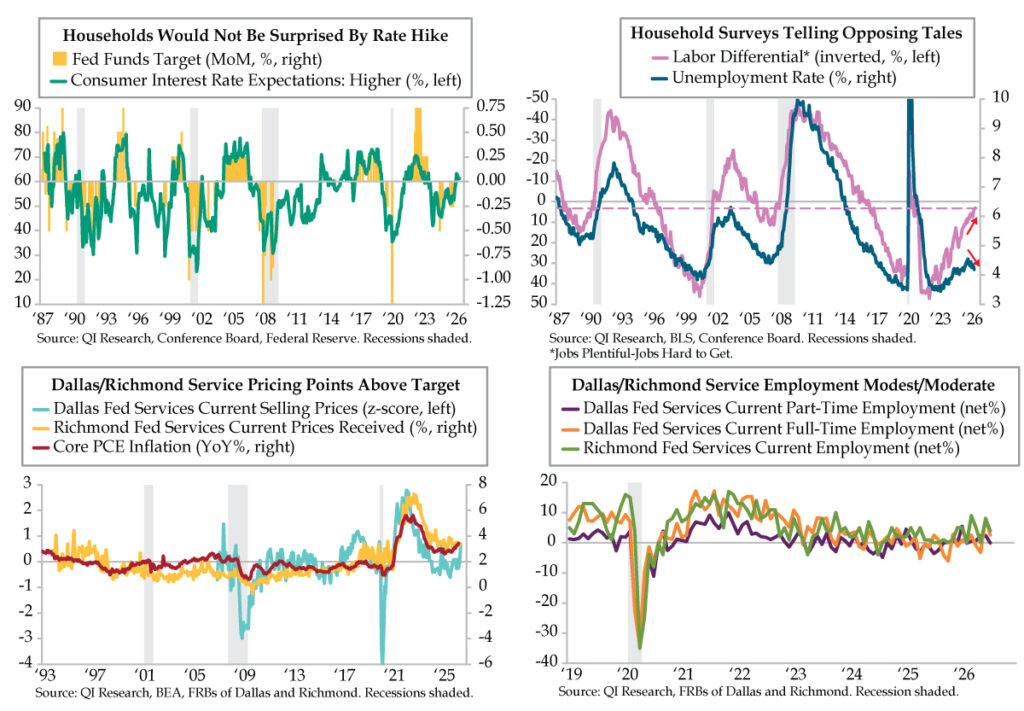

Celebrating Labor Liberty

Welcome to Quill Intelligence Please sign in or hit subscribe above. Thank you for visiting, The Quill Intelligence Team Login

That’s A Lot of Bull

Welcome to Quill Intelligence Please sign in or hit subscribe above. Thank you for visiting, The Quill Intelligence Team Login

Piletti, Not McFly

Welcome to Quill Intelligence Please sign in or hit subscribe above. Thank you for visiting, The Quill Intelligence Team Login

Infinite Gaps Don’t Apply

Welcome to Quill Intelligence Please sign in or hit subscribe above. Thank you for visiting, The Quill Intelligence Team Login

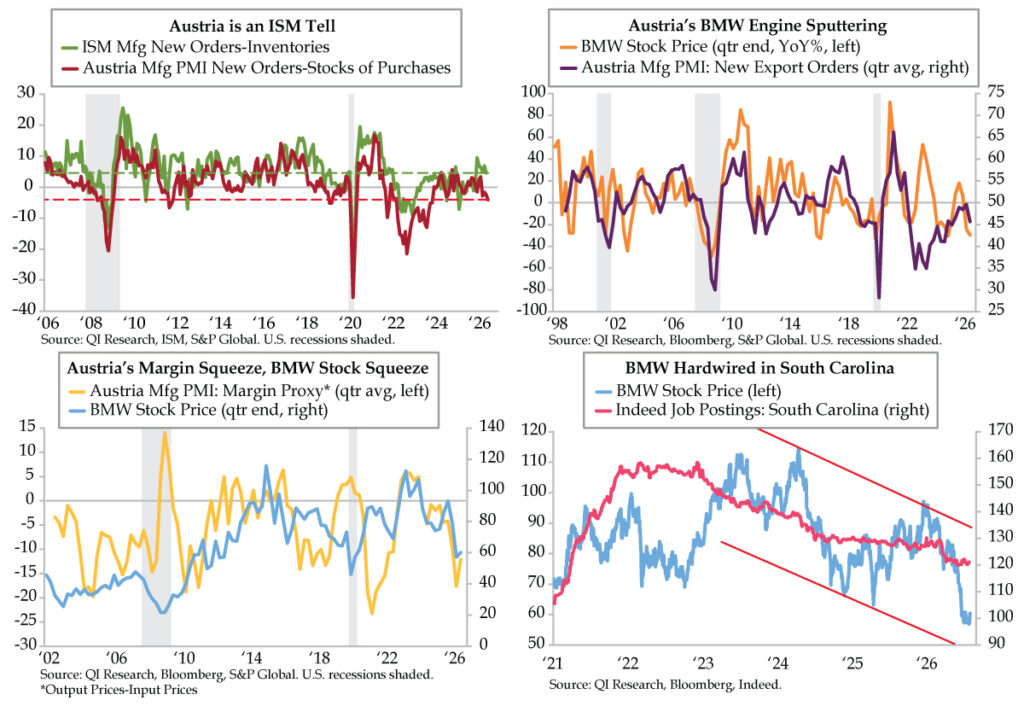

Beamer, Beemer, Bimmer

Welcome to Quill Intelligence Please sign in or hit subscribe above. Thank you for visiting, The Quill Intelligence Team Login

102 Dalmatians and an Oddball

Welcome to Quill Intelligence Please sign in or hit subscribe above. Thank you for visiting, The Quill Intelligence Team Login

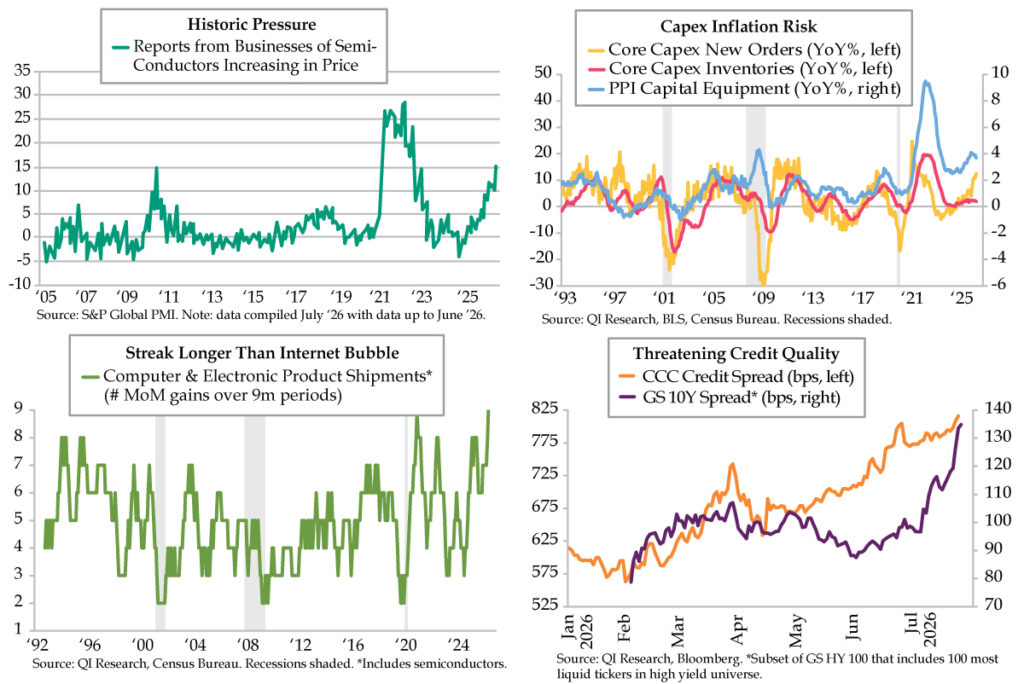

Aspect Ratios and Credit Quality

Welcome to Quill Intelligence Please sign in or hit subscribe above. Thank you for visiting, The Quill Intelligence Team Login

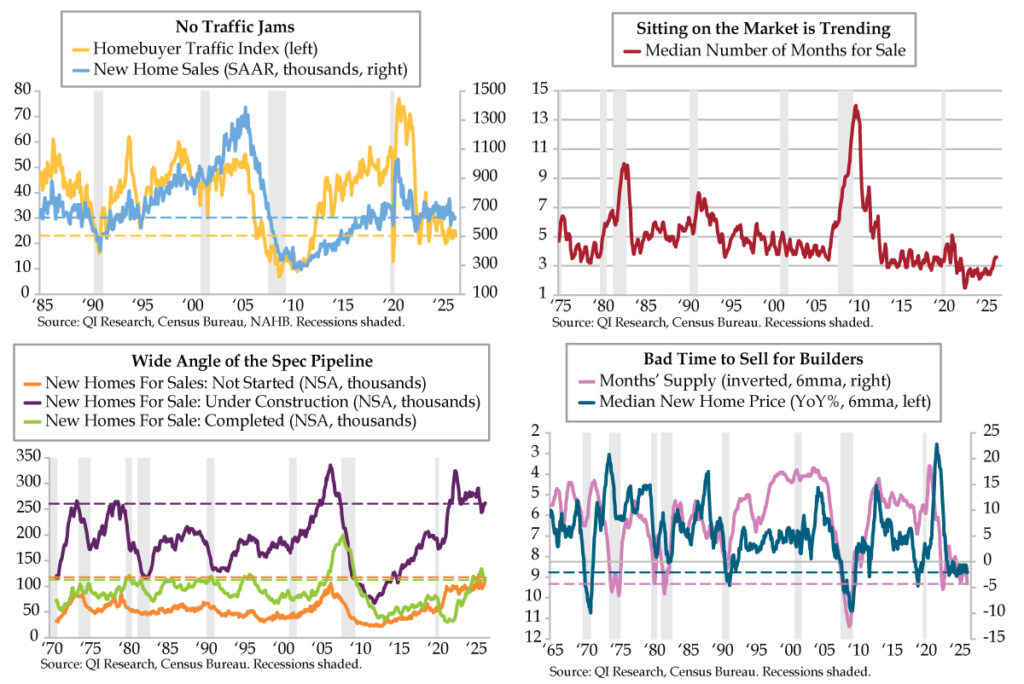

Leave Housing to Heaven

Welcome to Quill Intelligence Please sign in or hit subscribe above. Thank you for visiting, The Quill Intelligence Team Login