QUICK QUILL — Lower recession probability prompted by brightening expectations in Germany is a green shoot worth monitoring. Back in the States, consumer purchasing power has darkened as income gains wither amidst job cuts even as essentials inflation refuses to abate. The ‘tell’ would be slower consumer spending growth that threatens to fall to such an extent we hear more reports of U.S. households reducing the volume of groceries they can afford to buy. Until Powell sees the whites of the eyes of an unemployment rate with a 4-handle, TIPS investors will have to wait longer to back up the truck and become bullish.

TAKEAWAYS

- The consensus expects headline PCE to hold at 0.3% MoM in April while core PCE falls a tenth to 0.2% MoM; however, UMich’s preliminary May data gave no signs of cooling, with Bad News about Higher Prices climbing to a 6-month high of 17%, tripling the 5% average

- From Q1’s local high of 48.7, the UMich News Heard-Higher Unemployment Expectations spread has since more than halved to 20.0 in May; the downshift suggests real consumer spending has more room to fall after slipping from 2.7% YoY in Q4 2023 to 2.4% in Q1 2024

- TIP, the largest Treasury Inflation-Protected Securities bond ETF, is currently trading well below its post-pandemic highs; so long as Powell is able to point to the lack of forward progress on Supercore as reason to remain Higher for Longer, this looks set to continue

Of the forty hard jobs listed by CareerAddict.com for 2023, two stood out as especially life-threatening – cell tower climber and explosive ordnance disposal specialist. When scaling a tower, you could certainly fall, get your hand crushed, or even get struck by lightning. Detonating or diffusing live bombs would seem to be self-explanatory. Should you cut the red or the blue wire? If it wasn’t your bread & butter, you could romanticize about starring in your own Mission Impossible. In 2005, Staples introduced a fictional fix for real-life dangerous day jobs. It’s advertising agency, McCann Erickson depicted challenging tasks, like a cowboy wrangling a bucking horse and a father changing his twin infants’ diapers. In each case, pushing an “Easy Button” did the trick. The baritone voice-over would then say, “Wouldn’t it be nice if there was an Easy Button for life? Now there’s one for your business. Staples. That was easy.”

In 2008, Staples revived the campaign to “tackle” high prices. In each spot, a shopper is appalled at the price quoted for their purchase — whether gasoline, food, or clothing. The solution: Push the Easy Button and ask if that would make it any less expensive. Needless to say, the answer was always no. The post-pandemic era has been woefully bereft of Easy Button opportunities, even in jest. In the case of the United States, fiscal stimulus gone wild trained countless consumers to live beyond their means for “free,” and continue to do so using debt. In Europe, while there was less in the way of fiscal assistance, relatively stronger strictures on job cutting have helped.

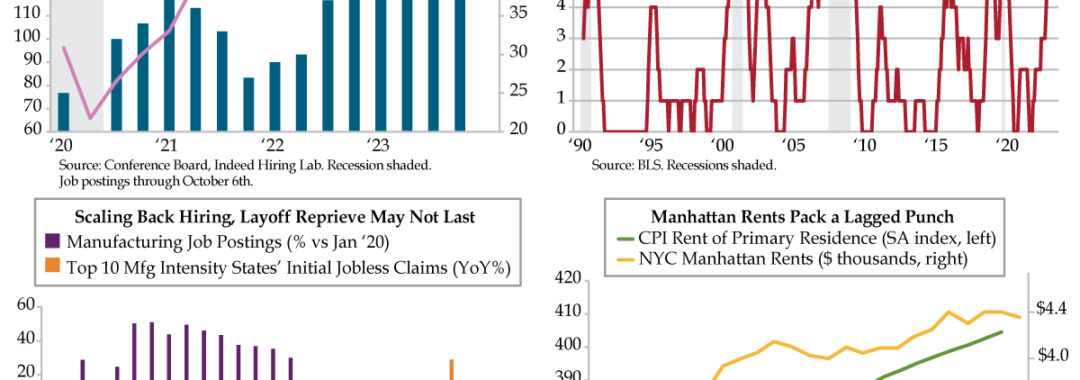

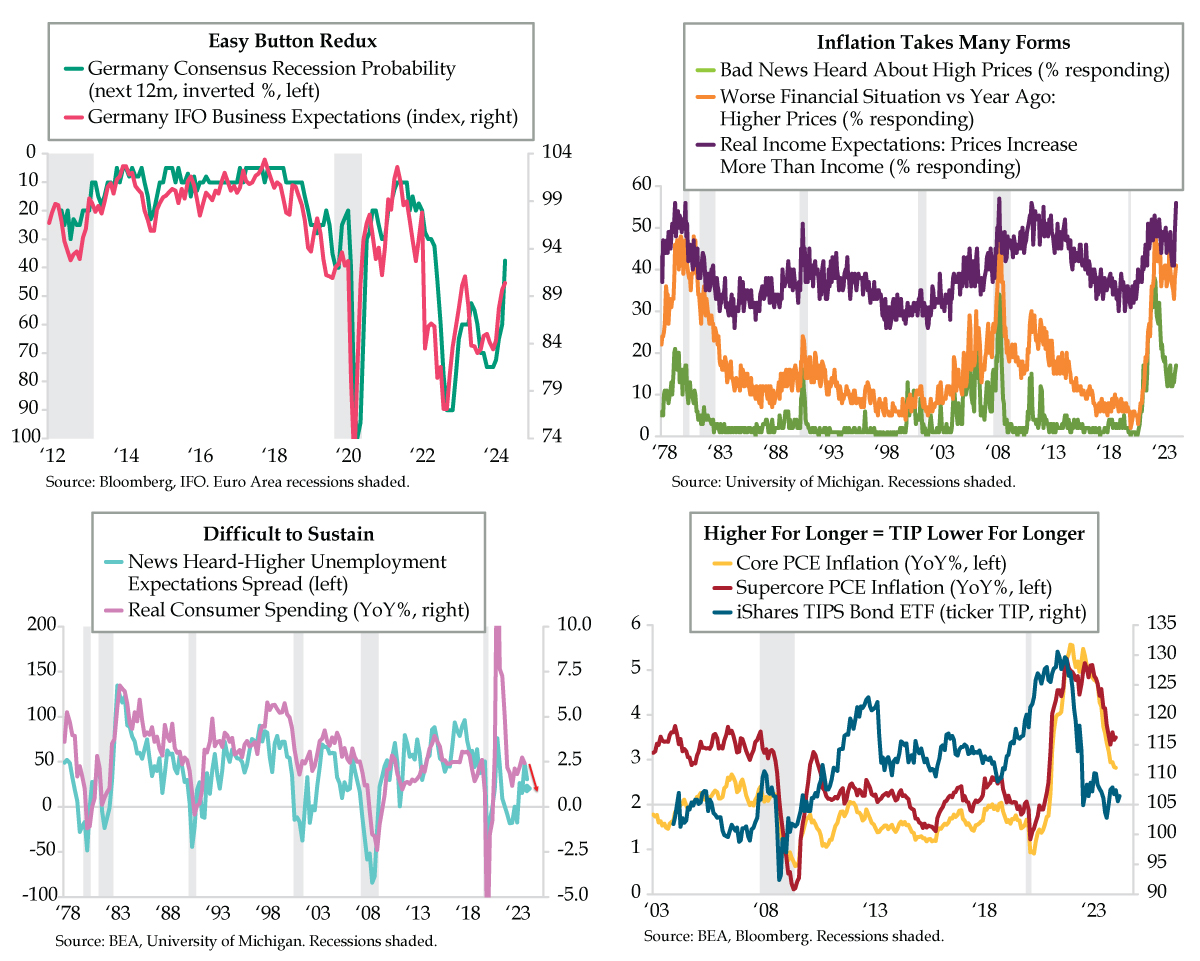

As for inflation, households on both sides of the pond have been largely helpless to fend off inflation over which their respective central banks hold little sway, particularly that of food and energy. Any good news is greeted with open arms as was the case with yesterday’s release of IFO Business Expectations (fuchsia line). Not only does it have an uncannily accurate relationship with recession probabilities in Deutschland (inverted teal line), expectations brightened to such an extent, they sent recession odds under 50% for the first time in two years.

Closer to home heading into a holiday-shortened trading week, the Federal Reserve’s preferred inflation gauge holds the most potential to move markets when it’s released Friday. Consensus is calling for April’s headline personal consumption expenditures (PCE) price index to stay steady with that of March – holding at 0.3% month-over-month (MoM) and 2.7% year-over-year (YoY). The core PCE, however, is expected to cool a tenth to 0.2% MoM, which would maintain its annual pace at 2.8% YoY (yellow line).

Last Friday’s University of Michigan (UMich) preliminary May consumer survey refuted any notion of cooling. Unfavorable News Heard About Higher Prices rose two points to a 6-month high of 17%, more than three times its 5% long-run average (green line). An elevated 41% said their Current Financial Situation had worsened due to higher prices, more than 17% norm (orange line).

Finally, a near record 56% believe price increases will more than offset income growth in the next year (purple line). There is decidedly more afoot than rising prices given May’s downticks for 1-year and 5-10-year UMich Inflation Expectations. The 15-point, two-month vault is unprecedented since the series 1978 inception.

The missing link: PRICING POWER. It’s not that inflation in isolation has resurged, so much as it being a case of inflation not keeping up with diminished incomes as job losses mount. Recall last week’s “Guardians of Gaslighting,” highlighted a Harris poll covered by The Guardian which found 49% of Americans “wrongly” thought the unemployment rate was at a 50-year high instead of it being the opposite case.

Not reporting true labor market data has apparently begun to grate on working Americans. Imagine that. In the meantime, two-thirds of U.S. economic output is comprised of consumption fueled by shrinking paychecks in the aggregate. Given surging credit card charge-offs, absent a continued spike in Buy Now Pay Later, we look to the spread between UMich News Heard-Higher Unemployment Expectations as a guide. It combines all buckets about recent changes in business conditions and contrasts it with households’ fear concerning future job loss. After 2024’s first quarter local high of 48.7, this metric has more than halved to May’s reading of 20.0 (aqua line). Heeding to pressures emanating from the labor market, the trend in real consumer spending already has eased from 2.7% YoY in 2023’s fourth quarter to 2.4% in 2024’s first quarter (lilac line).

Will policymakers at the Fed, who will put us out of our misery by entering FOMC blackout come Friday, be swayed by collapsing household perceptions of the job market? We doubt that seriously. Tourists would agree – that is, passive investors in the asset class designed to protect against inflation. The largest Treasury Inflation-Protected Securities bond exchange-traded fund, ticker TIP, is still trading well below its post-pandemic highs (blue line). The price of TIP is effectively the mirror image of real rates staying Higher for Longer to combat core inflation, which we’ve been told is too sticky and too steep for policymakers’ liking. To be sure, idiosyncrasies attendant to the vagaries of insurance rates and other sources of inflation out of the Fed’s control have stalled disinflation in Supercore PCE (red line). Such realities still won’t prompt Powell et al to whip out the Ease Button.